Your contractor just finished installing your new kitchen cabinets but disappeared after you discovered water damage from improperly sealed plumbing connections beneath the sink, leaving you facing a twelve-thousand-dollar repair bill with no way to recover your losses until you remember seeing “Licensed and Bonded” on their business card and wonder whether that cryptic phrase might actually provide financial recourse for the shoddy workmanship that’s now threatening your home. Understanding what license and permit bonds actually protect, who they’re designed to benefit, and how to file claims against contractors or businesses that fail to meet their obligations could mean the difference between eating the entire cost of someone else’s mistakes and recovering every dollar you’re owed through a financial guarantee mechanism specifically created to protect consumers like you from exactly this scenario.

A license and permit bond is a type of financial guarantee required by government agencies as a condition for granting business licenses or permits, ensuring that businesses comply with all applicable laws, regulations, and ethical standards related to their operations while providing financial recourse for consumers and governing bodies harmed by unethical practices, fraud, or legal violations. These bonds represent three-party agreements among principals who purchase bonds to obtain licenses, obligees who require bonds for consumer protection, and surety companies who guarantee principals’ compliance with regulatory requirements. License and permit bonds protect everyone except the party purchasing them, creating legally binding obligations requiring bonded businesses to reimburse surety companies for all claim payments made to injured consumers or regulatory authorities when businesses violate licensing laws, abandon contracted work, commit fraud, or otherwise fail to meet professional obligations.

The fundamental characteristic distinguishing license and permit bonds from all other business requirements involves the mandatory protection flowing away from bond purchasers toward the public they serve. When you as a contractor, auto dealer, mortgage broker, or other licensed professional purchase a license or permit bond, you receive absolutely no protection for yourself under the bond arrangement. Instead, the bond exists solely to protect your customers, clients, and the general public from your failures to comply with regulatory requirements, perform contracted work according to industry standards, or operate your business ethically within legal boundaries established by licensing authorities. This counterintuitive reality means businesses pay premiums for financial products designed exclusively to protect their clients, customers, regulators, and communities rather than themselves.

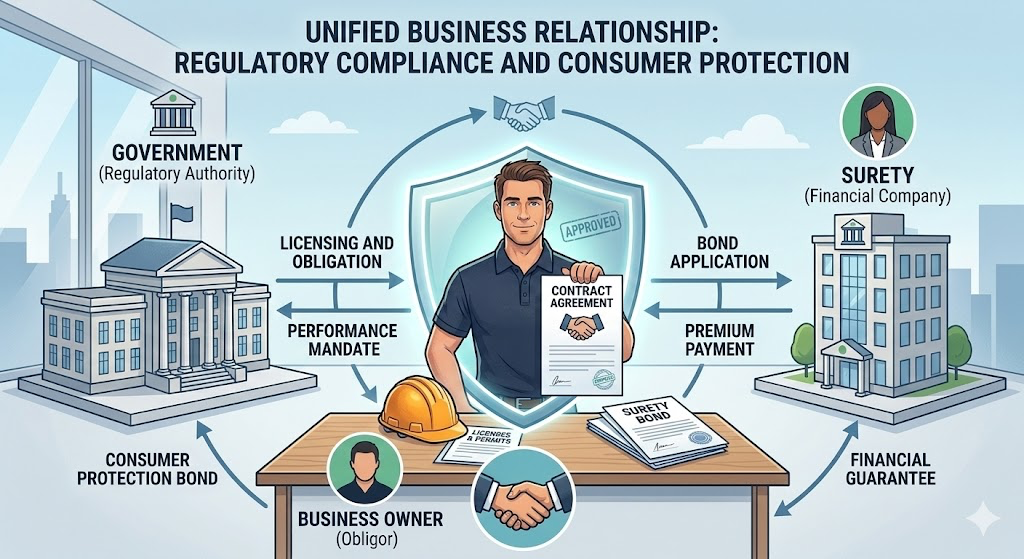

The Three-Party Structure That Defines License and Permit Bonds

Every license and permit bond creates a triangular relationship among three distinct parties with different roles, rights, and obligations under the bonding agreement.

The principal represents the individual or business purchasing the license or permit bond and assuming complete financial responsibility for all obligations guaranteed under the bond. You as the principal pay bond premiums to obtain coverage but receive no protection for yourself, as the bond exists solely to protect others from your failures to comply with licensing laws, perform contracted work competently, or operate your business according to regulatory standards. Principals could be contractors seeking building permits, auto dealers applying for dealership licenses, mortgage brokers obtaining state authorization to originate loans, notaries public registering with counties, freight brokers securing federal operating authority, or any other business or professional required to provide financial guarantees to licensing authorities or regulatory agencies. When you sign bond applications and indemnity agreements as a principal, you create unlimited personal and corporate liability requiring you to reimburse sureties for every dollar they spend on claims plus all investigation costs, legal fees, and interest charges accruing from payment dates until you satisfy all reimbursement obligations.

The obligee is the government agency, licensing board, regulatory authority, or public body requiring the bond as a condition of granting licenses or permits authorizing business operations in regulated industries. Obligees could include state contractor licensing boards requiring construction bonds, departments of motor vehicles requiring auto dealer bonds, mortgage regulatory agencies requiring lender bonds, county clerks requiring notary bonds, or city building departments requiring permit bonds for specific construction projects. These entities mandate bonds to ensure businesses operate according to established rules protecting public safety and consumer interests, providing immediate financial recourse for consumers harmed by bonded professionals’ misconduct without requiring injured parties to pursue lengthy litigation against businesses that might lack resources to compensate victims. The obligee benefits from financial guarantees that principals will fulfill regulatory obligations regardless of principals’ financial conditions, business failures, or deliberate violations of licensing requirements.

The surety company issues bonds guaranteeing principals’ regulatory compliance and professional obligations to obligees after evaluating principals’ creditworthiness, financial strength, business experience, and likelihood of generating claims requiring surety intervention. Sureties maintain the financial reserves and legal authority to pay consumer claims on principals’ behalf when bonded businesses violate licensing laws, abandon contracted work, commit fraud, or otherwise fail to meet obligations guaranteed under bonds. Unlike insurers who expect to absorb claim costs as part of their business models and pool premiums from many policyholders to fund anticipated losses, sureties pursue complete reimbursement from principals for every dollar paid on claims plus all associated investigation costs, legal fees, and interest charges through indemnity agreements creating legally enforceable debt obligations. The surety expects the principal will comply with all licensing requirements and perform all contracted obligations faithfully, pricing bonds at rates far below comparable insurance coverage because sureties don’t build reserves to fund claim payments the way insurers do.

How License and Permit Bonds Differ From Commercial Insurance

While surety companies that issue license and permit bonds are typically insurance carriers, license and permit bonds are not insurance products despite sharing some superficial similarities in premium collection and claim payment processes.

Commercial insurance policies create two-party contracts between businesses purchasing coverage and insurance companies providing protection, transferring risks of unpredictable events like fires, accidents, professional errors, or lawsuits from policyholders to insurers who absorb losses without expecting repayment. When your general liability insurance pays a fifty-thousand-dollar slip-and-fall claim after a customer trips on debris at your construction site, you don’t owe your insurer fifty thousand dollars because the insurer absorbed that loss as part of the risk they assumed when issuing your policy. Insurance premiums are designed to fund future claim payments across entire policyholder pools, with insurers collecting regular payments from many customers to create reserves covering losses suffered by the few experiencing covered events. The insurance company invests these pooled funds to generate returns while maintaining sufficient liquidity to pay claims as they arise, pricing premiums to reflect actuarial calculations estimating the likelihood and severity of claims your business might generate based on your industry, operations, claims history, and risk characteristics.

License and permit bonds establish three-party agreements among principals purchasing bonds, obligees requiring bonds for public protection, and surety companies guaranteeing principals’ regulatory compliance and professional obligations, functioning as credit instruments where sureties temporarily pay consumer claims but then aggressively pursue full reimbursement from principals who remain ultimately liable for all amounts paid plus investigation costs, legal fees, and interest accruing until principals satisfy all debts owed to sureties. When sureties pay claims to compensate consumers for principals’ failures to meet licensing requirements or perform contracted work competently, they immediately turn to principals demanding complete reimbursement under indemnity agreements signed when bonds were obtained. These indemnity agreements create legally binding obligations requiring principals to repay sureties every dollar spent on claims regardless of whether principals have the financial resources to make payments.

The reimbursement demand includes not just the claim amount paid to injured consumers but also all costs sureties incurred investigating claims, legal fees for attorneys who reviewed bond language and advised on surety obligations, costs of arranging completion contractors if sureties chose that remedy for abandoned construction projects, and interest accruing from payment dates until principals reimburse all amounts owed. Principals who cannot immediately reimburse sureties face aggressive collection actions including lawsuits, liens against business and personal assets, garnishment of accounts, pursuit of personal guarantees from business owners and their spouses who co-signed indemnity agreements, and potentially business liquidation or personal bankruptcy if debts cannot be repaid through normal business operations or asset sales.

License and permit bonds protect third parties requiring guarantees from principals’ failures to meet regulatory obligations or perform contracted work competently, with sureties expecting to recover all claim payments from principals through reimbursement creating contingent liabilities that can threaten business survival and personal financial security. Commercial insurance protects the party purchasing coverage from unpredictable losses they suffer due to accidents, errors, or disasters, with insurers absorbing claim costs without expecting policyholders to reimburse paid amounts. This fundamental difference explains why bonds cost substantially less than insurance for comparable coverage amounts and why strong credit and solid financials prove essential for obtaining bonds at reasonable rates.

The Two Main Categories of License and Permit Bonds

License and permit bonds serve distinct purposes with license bonds typically required on annual terms applying to all work performed under licensed authority while permit bonds are required on per-project bases for specific construction activities or temporary business operations.

License bonds guarantee that businesses holding professional licenses or operating authorities will comply with all laws, regulations, codes, and ethical standards governing their licensed activities throughout the bond term, typically one year corresponding with annual license renewal cycles. Government agencies at federal, state, county, or municipal levels require license bonds before issuing authorizations allowing businesses to operate legally in regulated industries. License bond requirements apply broadly across diverse business sectors including construction trades requiring contractor licenses with bonds guaranteeing compliance with building codes and consumer protection laws, automotive sales requiring dealer licenses with bonds guaranteeing proper title transfers and tax remittances, financial services requiring mortgage broker licenses with bonds guaranteeing compliance with lending regulations, professional services requiring notary bonds guaranteeing proper document authentication procedures, transportation requiring freight broker bonds guaranteeing payment to motor carriers, and countless other industries where government oversight protects public interests from business misconduct. License bonds remain active throughout annual license periods, applying to all business activities conducted under licensed authority rather than individual projects or transactions.

Permit bonds guarantee that businesses or property owners conducting specific activities will comply with applicable codes and regulations, complete permitted work according to approved plans, and repair any damage to public property like streets or sidewalks caused during permitted activities. Municipal building departments, county planning agencies, or state regulatory authorities require permit bonds before issuing authorizations for construction projects, special events, temporary business operations, or activities affecting public rights-of-way. Permit bond types include right-of-way bonds guaranteeing repair of damage to roads or sidewalks during utility installations or construction activities, encroachment permit bonds required for work within state rights-of-way like highway access driveways or grading projects affecting drainage patterns, special event permit bonds required for parades, races, festivals, or other temporary gatherings requiring street closures or public property use, and construction permit bonds required for building projects ensuring code compliance and proper site restoration. Permit bonds typically remain active for project durations or event dates rather than annual cycles, terminating when permitted work completes satisfactorily and authorities release bond obligations.

Common Types of License Bonds Across Industries

License bond requirements vary dramatically across industries and jurisdictions, with some businesses requiring multiple bond types to operate legally in different states or engage in various regulated activities.

Contractor license bonds represent the most common license bond type, required by most states and many municipalities for general contractors, specialty contractors, and construction trades including electricians, plumbers, roofers, HVAC contractors, paving contractors, demolition contractors, fencing contractors, landscapers, and numerous other building professionals. These bonds guarantee contractors will comply with building codes, obtain required permits, pay subcontractors and suppliers for incorporated labor and materials, complete contracted work according to specifications, and follow all laws governing construction activities. Bond amounts vary widely from five thousand dollars in some jurisdictions to one hundred thousand dollars or more in others, with most falling between ten thousand and twenty-five thousand dollars. Contractor license bonds protect homeowners and property owners from financial losses caused by contractor abandonment, code violations, unpaid subcontractors, or other failures to meet professional obligations.

Auto dealer bonds ensure vehicle dealerships comply with state laws regarding vehicle sales, properly transfer titles to purchasers, remit sales taxes to state revenue departments, avoid selling stolen vehicles, and maintain dealership operations according to regulatory standards protecting consumers from fraud and unethical practices. Most states require auto dealer bonds ranging from ten thousand to one hundred thousand dollars depending on dealership types and annual sales volumes. These bonds protect consumers who purchase vehicles from licensed dealers, providing financial recourse when dealers fail to deliver clear titles, misrepresent vehicle conditions, or engage in fraudulent practices violating state motor vehicle codes.

Mortgage broker bonds guarantee mortgage brokers and lenders comply with state and federal lending regulations, disclose loan terms accurately to borrowers, avoid predatory lending practices, maintain proper licensing, and conduct business ethically within legal boundaries protecting consumers from mortgage fraud. Most states require mortgage broker bonds ranging from twenty-five thousand to five hundred thousand dollars depending on loan volumes and licensing tiers. These bonds protect consumers who work with licensed mortgage professionals, providing compensation when brokers violate lending laws, misrepresent loan terms, or engage in fraudulent activities harming borrowers.

Freight broker bonds required by the Federal Motor Carrier Safety Administration guarantee freight brokers will pay motor carriers for transportation services rendered according to contracted rates, maintain proper insurance coverage, comply with federal transportation regulations, and operate ethically within industry standards. The current federal requirement mandates seventy-five thousand dollar bonds for freight brokers seeking operating authority to arrange shipments between shippers and motor carriers. These bonds protect motor carriers who transport freight arranged by licensed brokers, ensuring payment for services even when brokers fail financially or refuse to pay contracted rates.

Additional common license bond types include notary bonds protecting the public from notary errors or misconduct, insurance agent and broker bonds guaranteeing compliance with insurance regulations, collection agency bonds protecting consumers from improper debt collection practices, sales tax bonds guaranteeing businesses will remit collected sales taxes to state revenue departments, money transmitter bonds protecting consumers using money transfer services, immigration consultant bonds protecting immigrants from fraudulent immigration assistance, and dozens of other specialized bonds required across diverse regulated industries.

Understanding Bond Costs and Premium Factors

License and permit bond premiums represent one-time upfront payments covering specific bond terms rather than ongoing monthly obligations like insurance, typically ranging from one-half percent to fifteen percent of bond amounts depending on applicants’ creditworthiness and bond risk characteristics.

The cost of a license or permit bond depends on several interrelated factors that sureties evaluate when underwriting bond applications and quoting premium rates.

Bond amount represents the most obvious cost driver, as premiums are calculated as percentages of total coverage amounts with higher bond amounts generating proportionally higher premium costs in most cases. A ten-thousand-dollar contractor license bond costs substantially less than a one-hundred-thousand-dollar auto dealer bond even when applicants have identical credit profiles and business qualifications, simply because the surety’s potential exposure differs by a factor of ten.

Credit scores dramatically impact premium rates, with applicants possessing strong credit scores above seven hundred typically paying premium rates between one-half percent and three percent of bond amounts while applicants with poor credit scores below six hundred face premium rates between five percent and fifteen percent of bond amounts or outright declinations from standard surety markets forcing them into specialty high-risk programs. An applicant with a seven-hundred-fifty credit score might pay one hundred fifty dollars annually for a ten-thousand-dollar contractor license bond quoted at one-and-a-half percent, while an applicant with a five-hundred-fifty credit score might pay one thousand dollars annually for the identical bond quoted at ten percent, demonstrating how credit quality influences bonding costs by factors of five to ten times for otherwise identical situations.

Business experience and claims history affect premium rates, with well-established businesses operating for multiple years without bond claims qualifying for preferential rates while newly formed businesses or applicants with prior bond claims face higher rates reflecting increased risks. Sureties view established track records of regulatory compliance and satisfied customers as strong predictors of future performance, rewarding experienced applicants with lower premium rates while charging premium surcharges for unproven businesses or those demonstrating past failures to meet bonded obligations.

Bond type influences pricing as some license types involve higher claim frequencies or severities than others based on industry characteristics and regulatory enforcement patterns. Contractor license bonds typically generate more claims than notary bonds reflecting higher risks inherent in construction activities involving substantial sums and complex contractual relationships versus administrative document authentication services with limited financial exposures.

Financial strength demonstrated through business and personal financial statements affects underwriting decisions for larger bond amounts, with sureties examining working capital, debt levels, profitability, and asset quality when evaluating applications for bonds exceeding twenty-five thousand dollars. Applicants with strong balance sheets showing positive working capital, manageable debt ratios, and consistent profitability receive more favorable premium quotes than applicants with negative working capital, excessive leverage, or inconsistent earnings suggesting financial distress that could lead to business failures triggering bond claims.

How to Get Your License and Permit Bond

Obtaining your license and permit bond begins with identifying the specific bond type and coverage amount required by the licensing authority or regulatory agency specified in licensing statutes, permit applications, or regulatory correspondence you’ve received. Contact specialized surety bond agencies like Swiftbonds that maintain relationships with multiple surety companies capable of issuing various bond types across all fifty states and diverse industries, providing access to competitive markets and expert guidance navigating complex bonding requirements unique to your profession and jurisdiction.

The application process involves submitting documentation including personal and business tax returns, financial statements showing assets and liabilities, personal financial statements for business owners, credit authorization forms allowing sureties to pull credit reports, business licenses or professional certifications, and details about the specific license or permit you’re seeking. Sureties underwrite applications by evaluating creditworthiness through credit scores, analyzing financial strength through balance sheet review, examining business experience and professional qualifications, and reviewing specific regulatory requirements you must satisfy. Once underwriting concludes, sureties provide premium quotes typically ranging from one-half percent to three percent of bond amounts for qualified applicants with strong credit and established businesses, with higher rates for applicants facing credit challenges or operating newer ventures. After accepting quoted terms and paying premiums, you receive bond documents that must be filed with obligees according to their specified procedures and deadlines to satisfy bonding requirements and obtain licenses or permits authorizing your business operations.

Swiftbonds LLC

2024 Surety Bond Provider of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

Benefits of Maintaining License and Permit Bonds

Beyond satisfying mandatory regulatory requirements, license and permit bonds provide several strategic advantages enhancing business competitiveness and market positioning.

Consumer confidence increases dramatically when businesses advertise being “licensed, bonded, and insured” as this terminology signals to potential customers that businesses have undergone vetting by sureties willing to guarantee their work quality and regulatory compliance. Customers choosing between multiple service providers frequently select bonded contractors over non-bonded competitors even when bonded contractors charge higher prices, recognizing that bond protection provides financial recourse if work quality proves deficient or contractors abandon projects. This consumer preference for bonded businesses creates competitive advantages justifying premium pricing and generating higher close rates on sales opportunities.

Regulatory compliance avoidance of penalties demonstrates clear business value as operating without required bonds exposes businesses to substantial fines, license revocations, criminal charges in some jurisdictions, and lawsuits from customers discovering businesses operated illegally when harm occurred. The cost of bond premiums ranging from hundreds to thousands of dollars annually pales compared to penalties potentially reaching tens of thousands of dollars plus legal fees defending against enforcement actions and civil litigation.

Access to higher-value opportunities expands significantly with bonding capacity as many commercial projects, government contracts, and institutional clients require contractors or service providers to demonstrate bonding capability before submitting bids or proposals. Contractors without established surety relationships cannot compete for these opportunities regardless of their technical qualifications or competitive pricing, effectively excluding them from market segments representing substantial revenue potential. Building strong surety relationships through consistent premium payments, timely renewals, and clean claims histories establishes bonding capacity enabling businesses to pursue larger projects and more lucrative contracts driving revenue growth and business expansion.

Professional credibility enhancement occurs when businesses maintain bonds for extended periods demonstrating stability and financial responsibility to customers, suppliers, subcontractors, and lending institutions. Sureties conduct rigorous underwriting before issuing bonds, evaluating creditworthiness, financial stability, and professional qualifications, so maintaining active bonds signals that independent third-party financial institutions have verified your business merits their confidence. This third-party validation enhances your professional reputation beyond what self-certification or marketing claims could achieve.

Consequences of Operating Without Required Bonds

Businesses operating without required license or permit bonds face severe consequences affecting their legal standing, financial stability, and long-term viability.

License revocation or denial represents the most immediate consequence as licensing authorities will not issue new licenses or renew existing licenses until applicants satisfy all bonding requirements. This effectively shuts down business operations in regulated industries where licensing represents a legal prerequisite for conducting business, forcing businesses to cease operations until they obtain required bonds.

Criminal charges may apply in some jurisdictions where operating without required licenses and bonds constitutes criminal violations punishable by fines and potentially jail time for business owners. While many jurisdictions treat unlicensed operations as civil matters resulting in administrative penalties, some states classify unlicensed contracting or other regulated activities as criminal misdemeanors or felonies depending on transaction values and harm to consumers.

Civil lawsuits from customers discovering businesses operated without required bonds frequently result in judgments exceeding the actual damages suffered as courts may award punitive damages or attorney fees on top of compensatory damages when businesses knowingly violated licensing requirements. A customer suffering ten thousand dollars in damages from defective work might recover thirty thousand dollars or more in total judgments when proving the contractor operated without required licensing and bonding, with courts viewing licensing violations as aggravating factors justifying enhanced damages.

Financial penalties assessed by regulatory authorities range from hundreds to tens of thousands of dollars per violation depending on jurisdictions and violation severity. Operating for extended periods without required bonds can generate multiple violations as each day of unlicensed operation or each transaction conducted without proper bonding might constitute separate violations subject to individual penalties, creating exposure to cumulative fines potentially bankrupting businesses.

Permanent business damage occurs even after resolving immediate legal issues as regulatory enforcement actions become public records accessible to potential customers researching businesses online. Past license suspensions or revocations appear in background checks, online reviews reference enforcement actions, and competitors use licensing violations as competitive ammunition discrediting businesses in the marketplace. This reputational damage can persist for years after businesses resolve their compliance issues and obtain proper bonding.

Frequently Asked Questions

What happens if I need to file a claim against a bonded contractor who abandoned my project?

Filing claims against license or permit bonds requires documenting the bonded principal’s violation of licensing laws or failure to meet contractual obligations, submitting written claim notices to surety companies within specified timeframes often ranging from one to three years from violation dates depending on jurisdictions, and providing evidence supporting claim validity including contracts, invoices, photographs, expert reports, and correspondence demonstrating the principal’s failures. Sureties investigate claims by reviewing submitted documentation, contacting principals to obtain their perspectives on disputed matters, potentially hiring independent experts to assess technical aspects of construction defects or regulatory violations, and determining whether valid claims exist under bond terms. If sureties conclude claims are valid, they may attempt facilitating resolutions between claimants and principals before paying claims, or they may pay claims directly to claimants up to bond amounts and then pursue reimbursement from principals through indemnity agreements. The claim process typically takes thirty to ninety days from initial filing through resolution depending on claim complexity and dispute levels, with more straightforward abandoned project claims resolving faster than technical construction defect claims requiring expert evaluations. Remember that bond amounts cap total available recovery, so if multiple claimants file against the same bond, available funds may be exhausted before all valid claims receive full compensation.

Can I get license and permit bonds if I have bad credit or past bankruptcies?

Obtaining license and permit bonds with poor credit, low credit scores below six hundred, or recent bankruptcies within the past five to seven years proves extremely difficult but not impossible through specialized high-risk surety programs willing to work with applicants standard markets decline. Standard surety markets typically decline applicants with credit scores below six hundred, bankruptcies within the past seven years, past bond claims, significant financial weaknesses like negative working capital or excessive debt loads, tax liens, or civil judgments. Specialized high-risk sureties may still provide coverage but at dramatically higher premium rates potentially reaching ten to twenty percent of bond amounts instead of the one to three percent that strong applicants pay with excellent credit. Some high-risk programs require collateral such as cash deposits equal to bond amounts, letters of credit from banks, or pledges of business or personal assets securing the surety’s position and providing immediate recourse if claims arise. Indemnitors with strong finances unrelated to your business such as creditworthy relatives or business partners might be required to co-sign indemnity agreements guaranteeing bonds and accepting joint liability for reimbursement obligations. Past bond claims create particularly difficult underwriting challenges since they demonstrate exactly the performance failures that bonds guarantee against, making sureties extremely reluctant to extend new credit to principals who previously defaulted on bonded obligations. Working with surety specialists experienced in high-risk markets and willing to advocate for your application provides the best chance of securing coverage when you face credit challenges.

How do license and permit bonds differ from contractor insurance policies?

License and permit bonds and contractor insurance policies serve completely different functions with bonds protecting customers and the public from contractor failures to meet regulatory obligations or perform contracted work competently while insurance protects contractors from unexpected losses they suffer due to accidents, injuries, or property damage occurring during business operations. General liability insurance protects contractors from claims alleging bodily injury or property damage caused by contractors’ operations, such as customers tripping over construction debris or water damage to adjacent properties from contractor negligence, with insurance companies paying valid claims without expecting contractors to reimburse paid amounts. Workers compensation insurance protects contractors from claims by injured employees seeking medical treatment and lost wages, with insurance carriers paying all covered medical expenses and disability benefits directly to injured workers without contractors reimbursing insurers. Professional liability or errors and omissions insurance protects design professionals like architects or engineers from claims alleging professional negligence causing financial losses to clients, with insurers defending professionals in lawsuits and paying settlement or judgment amounts up to policy limits. These insurance products all protect the contractor or design professional purchasing coverage from losses they suffer or liabilities they face, with insurance companies absorbing claim costs as part of their business models. License and permit bonds protect customers, property owners, and the public from contractor failures to complete work, comply with codes, pay subcontractors, or meet other professional obligations, with sureties expecting to recover all claim payments plus costs from contractors through indemnity agreement enforcement. Contractors need both proper insurance protecting themselves from operational risks and required bonds protecting their customers from performance failures, as these products address completely different risks flowing in opposite directions.

Do license and permit bonds automatically renew each year or do I need to take action?

Most license and permit bonds operate as continuous obligations remaining active as long as principals pay renewal premiums when due, typically thirty to forty-five days before current bond terms expire, with surety agencies contacting principals well in advance providing renewal invoices and updated bond forms if needed. Continuous bonds eliminate the need for principals to request new bonds or file updated bonds with obligees each renewal cycle, as original bonds remain legally effective through successive renewal periods as long as premiums are paid and neither sureties nor principals cancel bonds according to notice procedures specified in bond terms. However, principals remain responsible for initiating premium payments as sureties have no obligation to continue coverage if renewal premiums go unpaid, potentially allowing bonds to lapse and licenses to expire if principals miss payment deadlines or ignore renewal notifications. Some licensing authorities require updated bond forms each renewal cycle even for continuous bonds, necessitating principals to obtain current bonds from sureties and file them with licensing agencies before license renewals process completely. Permit bonds typically terminate when permitted work completes and authorities release bond obligations rather than renewing annually, though permits for long-duration projects extending beyond one year may require bond renewals or extensions until work completes satisfactorily. Bond renewal premiums often change from initial terms if principals’ credit scores improved or declined, claim experience developed, bond amounts increased due to regulatory changes, or surety company rate structures adjusted, so renewal costs may differ substantially from original premiums requiring principals to budget appropriately for potential increases. If sureties discover during renewal underwriting that principals’ financial conditions deteriorated significantly, past-due tax obligations developed, or other risk factors emerged since initial bonding, sureties may decline renewals forcing principals to seek coverage from different sureties potentially at much higher costs or with collateral requirements.

What’s the difference between fixed bond amounts and ranged bond amounts for license requirements?

Fixed bond amounts mean the same coverage amount applies to all applicants seeking specific license types regardless of business size, revenue volume, or operational scope, common with many contractor licenses, notary bonds, and other professional licenses where regulators determined a standard coverage amount provides adequate public protection across diverse business scales. For example, a state might require all general contractors to post fifteen-thousand-dollar license bonds whether contractors perform ten projects annually totaling two hundred thousand dollars or one hundred projects annually totaling twenty million dollars, with the identical bond amount applying equally to all licensed contractors in that classification. Fixed amounts simplify licensing administration as regulators don’t need to calculate individual bond requirements for each applicant, but they may provide insufficient protection for consumers hiring larger contractors whose potential to cause significant financial harm exceeds fixed bond amounts substantially. Ranged bond amounts mean required coverage varies based on applicant-specific factors like business revenue, transaction volumes, number of vehicles, number of employees, or scope of licensed authority, with regulators tailoring bond amounts to match risk exposures created by different business scales. For example, auto dealer bond requirements might range from twenty-five thousand dollars for dealers selling fewer than fifty vehicles annually to one hundred thousand dollars for dealers selling more than five hundred vehicles annually, with bond amounts scaling proportionally to sales volumes reflecting greater consumer exposure to potential harm from high-volume dealers. Ranged amounts provide more proportional protection matching bond coverage to actual risks but create additional administrative complexity as licensing authorities must verify revenue levels or other factors determining applicable bond amounts and applicants must document their business scales during licensing processes. Some bonds tie amounts to specific asset values like estate bonds required of administrators managing probate estates where bond amounts equal estate values to protect heirs from administrator malfeasance, or construction performance bonds where bond amounts equal project contract values to protect owners from contractor default.

Conclusion

License and permit bonds represent three-party financial guarantees required by government agencies as conditions for granting business licenses or permits, ensuring bonded businesses comply with all applicable laws, regulations, and ethical standards while providing financial recourse for consumers and regulatory authorities harmed by business failures to meet professional obligations. The three-party structure distinguishes bonds from all other financial products, creating triangular relationships among principals who purchase bonds and assume unlimited reimbursement obligations, obligees who require bonds for public protection, and sureties who issue bonds guaranteeing principals’ regulatory compliance while expecting complete recovery of all claim payments through aggressive reimbursement enforcement.

Understanding that license and permit bonds protect third parties rather than bond purchasers helps businesses appreciate the serious nature of indemnity obligations created when obtaining bonds to satisfy licensing requirements. The reimbursement requirement distinguishing bonds from insurance means bond claims create debt obligations principals must repay including claim amounts, investigation costs, legal fees, and interest, with collection actions potentially including lawsuits, asset liens, garnishments, and personal guarantees surviving business bankruptcies when business owners co-signed indemnity agreements.

The credit-based underwriting process focusing on principals’ ability to reimburse claims differs dramatically from insurance underwriting pricing policies based on expected loss frequencies and severities. This difference explains why bonds cost substantially less than comparable insurance coverage and why strong credit scores and solid financials prove essential for obtaining bonds at reasonable rates ranging from one-half percent to three percent for qualified applicants versus five percent to fifteen percent for applicants facing credit challenges.

License bonds and permit bonds serve distinct purposes with license bonds required on annual terms applying to all work performed under licensed authority while permit bonds required on per-project bases guarantee specific construction activities or temporary operations comply with codes and regulations. Common license bond types include contractor licenses, auto dealer licenses, mortgage broker licenses, freight broker licenses, notary bonds, and hundreds of specialized bonds required across regulated industries, with bond amounts ranging from small five-thousand-dollar bonds for individual professionals to large multi-million-dollar bonds for high-volume businesses creating substantial public exposure.

Maintaining required license and permit bonds provides strategic advantages beyond regulatory compliance including enhanced consumer confidence from advertising “licensed, bonded, and insured” status, penalty avoidance saving substantial fines and legal expenses, access to higher-value opportunities requiring demonstrated bonding capacity, and professional credibility enhancement through third-party validation of financial responsibility. Operating without required bonds exposes businesses to license revocations, criminal charges in some jurisdictions, civil lawsuits with enhanced damages, substantial financial penalties, and permanent reputational damage persisting long after resolving immediate compliance issues.

Five Hidden Realities About License and Permit Bonds

The medieval guild system of thirteenth-century Europe required master craftsmen to post monetary pledges with guild authorities before training apprentices or accepting commissioned work, creating the earliest documented predecessor to modern license and permit bonds where financial guarantees ensured craftsmen maintained quality standards and completed contracted work according to guild regulations. These pledges functioned identically to contemporary bonds with guild masters reimbursing authorities for customer complaints or abandoned work, though the system operated through informal community enforcement rather than formalized surety company structures that emerged centuries later during the Industrial Revolution when growing commercial complexity demanded standardized financial instruments replacing localized guild systems.

Many states allow applicants to satisfy license bond requirements through alternative mechanisms including cash deposits equal to bond amounts held by licensing agencies in interest-bearing accounts, certificates of deposit pledged to regulatory authorities as collateral, letters of credit from banks guaranteeing payment to licensing agencies upon demand, or participation in state-operated trust fund programs where businesses contribute to pooled funds compensating consumers for losses. These alternatives particularly benefit applicants who cannot obtain traditional surety bonds due to credit challenges or past claims, though cash deposits and certificates of deposit tie up working capital that could otherwise fund business operations while surety bonds allow businesses to preserve liquidity by paying small premiums instead of depositing full bond amounts.

Bond amount requirements for many license types established decades ago have never adjusted for inflation despite dramatic increases in construction costs, vehicle prices, and general cost of living that should theoretically drive proportional bond amount increases to maintain equivalent consumer protection levels. A contractor license bond set at fifteen thousand dollars in 1985 when average home prices were seventy-five thousand dollars represented twenty percent of home values, but that same fifteen-thousand-dollar bond in current markets where average home prices exceed four hundred thousand dollars represents less than four percent of home values, providing substantially diminished protection relative to potential consumer losses from contractor default or poor workmanship despite nominal bond amounts remaining unchanged.

Some jurisdictions structure license bonds as automatically renewing obligations requiring neither surety notices to cancel nor principal actions to renew, with bonds remaining perpetually active until either sureties provide written cancellation notices to licensing agencies typically requiring thirty to ninety days advance notice, or principals formally request bond cancellations and obtain official releases from licensing authorities. This automatic renewal structure benefits principals by eliminating risks that forgotten renewal deadlines might allow bonds to lapse causing license suspensions, though it also creates potential exposure to unexpected premium increases or changed bond terms at renewal that principals might miss without actively monitoring renewal correspondence from surety agencies managing their bond portfolios.

Certain high-risk industries face requirements for both license bonds protecting consumers from business failures and errors and omissions insurance protecting against professional negligence, creating dual layers of financial protection addressing different risk categories with bonds covering intentional misconduct, abandonment, or regulatory violations while insurance covers unintentional errors, omissions, or technical mistakes. For example, some states require mortgage brokers to maintain both fifty-thousand-dollar license bonds guaranteeing regulatory compliance and one-million-dollar errors and omissions insurance covering negligent loan origination mistakes, recognizing that bond coverage designed for fraud protection provides inadequate consumer compensation for negligence claims potentially exceeding bond amounts by factors of ten or twenty when defective loans cause foreclosures or substantial financial losses to borrowers relying on professional advice.

Leave a Reply