The general contractor you hired to renovate your office building just disappeared three months into a six-month project after receiving seventy percent of the contract payment, leaving you with an incomplete structure, unpaid subcontractors filing liens against your property, and a crushing realization that recovering your two-hundred-thousand-dollar loss through litigation could take years and cost nearly as much as the original contract amount until you remember the performance bond requirement in your contract and wonder whether this financial instrument might actually provide the immediate recourse you desperately need to complete your project and compensate your losses. Understanding what performance bonds guarantee, how the three-party surety relationship protects project owners from contractor default while creating serious reimbursement obligations for contractors who fail to complete work, and when these bonds are legally required versus strategically recommended could mean the difference between financial catastrophe and swift project completion when construction ventures fail to meet contractual obligations as originally promised.

A performance bond is a type of surety bond issued by insurance companies or banks guaranteeing satisfactory completion of construction projects by contractors according to terms outlined in contracts between contractors and project owners, ensuring project owners receive financial compensation or completion assistance when contractors default on obligations due to bankruptcy, abandonment, incompetence, or other failures to meet performance requirements. These bonds represent three-party financial agreements among principals who are contractors purchasing bonds to secure projects, obligees who are project owners or government agencies requiring bonds for protection, and sureties who are financial institutions guaranteeing contractors’ work while expecting complete reimbursement for any claim payments made to injured project owners when contractors fail to meet bonded obligations. Performance bonds protect project owners rather than bond purchasers, creating legally binding obligations requiring bonded contractors to reimburse surety companies for all claim amounts plus investigation costs, legal fees, interest charges, and completion expenses when contractors abandon projects, deliver defective work, violate building codes, or otherwise breach contractual commitments.

The fundamental characteristic distinguishing performance bonds from all other financial products involves the reimbursement requirement flowing from contractors back to surety companies after sureties pay claims to compensate project owners for contractor failures. When you as a contractor purchase a performance bond to satisfy project requirements, the bond exists solely to protect your client from your failures to complete work according to contract specifications, maintain project schedules, comply with building codes, or deliver quality meeting industry standards. This creates a counterintuitive financial relationship where you pay premiums for coverage that exclusively benefits others while exposing you to unlimited reimbursement liability when claims arise from your performance deficiencies.

The Ancient Origins and Modern Evolution of Performance Bonds

Performance bonds trace their origins to ancient civilizations dating back to 2,750 BC when Mesopotamian merchants required financial guarantees before engaging contractors for major construction projects or trade ventures. The Romans developed formal laws of surety around 150 AD establishing legal principles governing three-party guarantee relationships, contractor obligations, and surety rights that remain foundational to modern bonding practices twenty centuries later. These ancient Roman legal concepts established that sureties providing financial guarantees could pursue complete reimbursement from principals whose failures triggered guarantee payments, creating the indemnity principle distinguishing surety bonds from insurance products where policyholders never reimburse insurers for claim payments.

The United States Congress passed the Miller Act in 1932 during the Great Depression addressing a systemic problem plaguing federal construction projects where unscrupulous contractors deliberately underbid government contracts intending to abandon work or demand price increases after project commencement, essentially holding government agencies hostage with threats to walk away from partially completed infrastructure projects. Before Miller Act requirements, federal agencies faced impossible choices between paying inflated demands from contractors who reneged on original bids or terminating contractors and rebidding projects only to encounter identical problems with replacement contractors. The Miller Act solved this ransom situation by requiring performance and payment bonds for all federal construction contracts exceeding one hundred thousand dollars, ensuring only financially stable contractors capable of completing projects could bid on government work while providing immediate financial recourse when contractors defaulted on obligations.

Following federal success with Miller Act bonding requirements, states enacted “Little Miller Acts” establishing similar performance bond mandates for state-funded construction projects with varying threshold amounts and specific procedural requirements unique to each jurisdiction. These state-level bonding laws expanded performance bond usage beyond federal projects to encompass state highway construction, public school buildings, municipal infrastructure, and countless other government-funded construction activities requiring financial guarantees protecting taxpayer investments in public works.

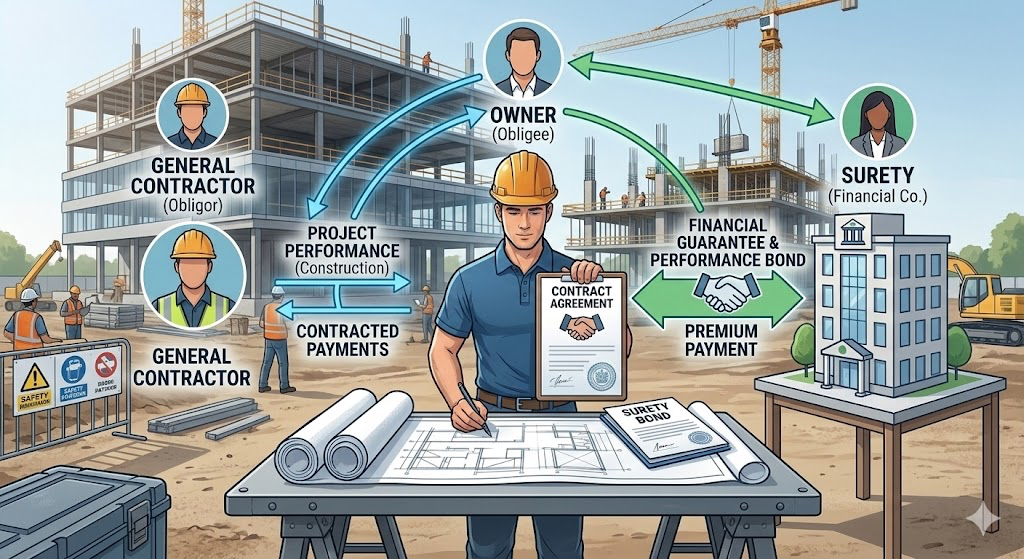

Understanding the Three-Party Surety Bond Structure

Every performance bond creates triangular relationships among three distinct parties with different roles, rights, obligations, and financial exposures under bonding agreements.

The principal represents the contractor or construction company purchasing the performance bond to satisfy project requirements and secure contracts from project owners or government agencies. You as the principal assume complete financial responsibility for all obligations guaranteed under the bond including project completion according to specifications, adherence to approved schedules, compliance with building codes and safety regulations, proper payment of subcontractors and suppliers, and correction of any defective work discovered during warranty periods. Principals could be general contractors bidding on commercial construction projects, specialty contractors performing specific trades like electrical or plumbing work, civil engineering firms handling infrastructure development, or any construction business required to provide financial guarantees to project owners. When you sign bond applications and indemnity agreements as a principal, you create unlimited personal and corporate liability requiring you to reimburse sureties for every dollar they spend on claims plus all investigation costs, legal fees, completion contractor expenses, and interest accruing from payment dates until you satisfy complete reimbursement obligations.

The obligee is the project owner, government agency, public authority, or private developer requiring the bond as a condition of awarding construction contracts and benefiting from financial protections when principals fail to meet contractual obligations. Obligees could include federal agencies administering infrastructure projects, state departments of transportation building highways, municipal governments constructing public facilities, school districts developing educational campuses, private developers creating commercial properties, or any entity investing capital in construction ventures requiring financial guarantees against contractor default. These entities mandate performance bonds to ensure contractors possess financial strength and professional competence to complete projects as specified, providing immediate compensation mechanisms when contractors abandon work, deliver substandard performance, violate codes, or otherwise breach contractual commitments without requiring obligees to pursue lengthy litigation against potentially insolvent contractors.

The surety company issues bonds guaranteeing principals’ contractual performance and completion obligations to obligees after evaluating principals’ creditworthiness, financial stability, construction experience, project management capabilities, and likelihood of generating claims requiring surety intervention. Sureties maintain financial reserves and legal authority to pay project owner claims on principals’ behalf when bonded contractors default on obligations, but unlike insurers who expect to absorb claim costs as part of business models, sureties pursue aggressive reimbursement from principals for every dollar paid on claims plus all associated costs through indemnity agreements creating legally enforceable debt obligations. The surety underwrites each bond application assessing whether the principal possesses sufficient financial resources, technical expertise, and management competence to complete the proposed project successfully without triggering claims, pricing bonds at rates reflecting perceived risk levels while refusing to issue bonds for contractors deemed unlikely to complete projects or repay potential claim amounts.

How Performance Bonds Differ Fundamentally From Construction Insurance

While surety companies issuing performance bonds are typically insurance carriers, performance bonds are not insurance products despite superficial similarities in premium collection processes and claim payment mechanisms.

Commercial insurance policies create two-party contracts between businesses purchasing coverage and insurance companies providing protection, transferring risks of unpredictable events like accidents, fires, storms, or professional errors from policyholders to insurers who absorb losses without expecting repayment. When your general liability insurance pays a one-hundred-thousand-dollar injury claim after a worker falls from scaffolding at your construction site, you owe your insurer nothing because the insurer absorbed that loss as part of the risk they assumed when issuing your policy. Insurance premiums are designed to fund future claim payments across entire policyholder pools, with insurers collecting regular payments from many customers to create reserves covering losses suffered by the few experiencing covered events during policy periods.

Performance bonds establish three-party agreements among principals purchasing bonds, obligees requiring bonds for project protection, and surety companies guaranteeing principals’ contractual performance, functioning as credit instruments where sureties temporarily pay project owner claims but then aggressively pursue full reimbursement from principals who remain ultimately liable for all amounts paid plus investigation costs, legal fees, completion expenses, and interest accruing until principals satisfy all debts owed to sureties. When sureties pay claims to compensate project owners for principals’ failures to complete projects according to contract specifications, they immediately turn to principals demanding complete reimbursement under indemnity agreements signed when bonds were obtained.

The reimbursement demand includes not just the claim amount paid to injured project owners but also all costs sureties incurred investigating claims, legal fees for attorneys who reviewed bond language and advised on surety obligations, costs of arranging completion contractors if sureties chose that remedy for abandoned construction projects, administrative expenses processing claims and pursuing collections, and interest accruing from payment dates until principals reimburse all amounts owed. Principals who cannot immediately reimburse sureties face aggressive collection actions including lawsuits seeking judgments, liens against business and personal assets, garnishment of bank accounts, pursuit of personal guarantees from business owners and spouses who co-signed indemnity agreements, and potentially business liquidation or personal bankruptcy if debts cannot be repaid through normal operations or asset sales.

When Performance Bonds Are Legally Required or Strategically Recommended

The Federal Miller Act mandates performance and payment bonds for all construction contracts issued by the federal government exceeding one hundred thousand dollars, requiring prime contractors to post bonds guaranteeing project completion and subcontractor payment before commencing any federally funded construction work. The current Miller Act appears in Title 40 of the United States Code, Chapter 31, Subchapter III, establishing detailed requirements for bond amounts, surety qualifications, claim procedures, and enforcement mechanisms protecting government interests in public construction projects.

State Little Miller Acts impose similar bonding requirements for state-funded construction projects with varying threshold amounts ranging from twenty-five thousand to one hundred thousand dollars depending on jurisdictions and project types. Some states require performance bonds for all public construction regardless of project size while others exempt smaller projects from bonding mandates, creating patchwork regulatory landscapes requiring contractors to understand specific requirements in each state where they operate. Municipal and county governments often adopt bonding ordinances requiring performance bonds for local public works projects including road construction, water system improvements, public building renovations, and infrastructure development funded by local tax revenues.

Private developers and commercial project owners increasingly require performance bonds even when not legally mandated, recognizing that bonding requirements provide multiple benefits beyond financial protection from contractor default. Private obligees requiring bonds gain assurance that bonded contractors have undergone rigorous financial underwriting by surety companies evaluating creditworthiness, construction experience, project management capabilities, and financial stability before issuing bonds. This third-party vetting reduces project owners’ risks of selecting financially unstable contractors likely to fail mid-project, potentially screening out undercapitalized businesses unable to complete projects successfully.

Large commercial construction projects, complex design-build ventures, public-private partnerships involving mixed funding sources, and high-value infrastructure developments frequently require performance bonds regardless of legal mandates as project owners seek maximum protection against contractor default on ventures representing substantial capital investments and tight completion schedules where delays create cascading financial consequences.

Understanding Performance Bond Costs and Premium Factors

Performance bond premiums represent percentages of total contract amounts rather than fixed fees, typically ranging from one percent to five percent of project values depending on contractors’ financial strength and bond risk characteristics.

The cost of a performance bond depends on several interrelated factors that sureties evaluate when underwriting bond applications and establishing premium rates.

Contract amount represents the most obvious cost driver, as premiums are calculated as percentages of total project values with higher contract amounts generating proportionally higher premium costs in most cases. A fifty-thousand-dollar renovation bond costs substantially less than a five-million-dollar commercial construction bond even when contractors have identical credit profiles and construction experience, simply because the surety’s potential exposure differs by a factor of one hundred.

Credit scores dramatically impact premium rates, with contractors possessing strong credit scores above seven hundred typically paying premium rates between one percent and three percent of bond amounts while contractors with poor credit scores below six hundred face premium rates between five percent and fifteen percent of bond amounts or outright declinations from standard surety markets forcing them into specialty high-risk programs charging premium surcharges. A contractor with a seven-hundred-fifty credit score might pay thirty thousand dollars annually for a one-million-dollar performance bond quoted at three percent, while a contractor with a five-hundred-fifty credit score might pay one hundred thousand dollars annually for the identical bond quoted at ten percent, demonstrating how credit quality influences bonding costs by factors of three to five times for otherwise identical situations.

Construction experience and claims history affect premium rates, with well-established contractors operating for multiple years without bond claims qualifying for preferential rates while newly formed construction businesses or contractors with prior bond claims face higher rates reflecting increased risks. Sureties view established track records of successful project completions and satisfied customers as strong predictors of future performance, rewarding experienced contractors with lower premium rates while charging premium surcharges for unproven businesses or those demonstrating past failures to meet bonded obligations.

Project type and complexity influence pricing as some construction categories involve higher claim frequencies or severities than others based on technical requirements and risk exposures. Simple renovation projects typically generate fewer claims than complex design-build ventures requiring sophisticated engineering, specialized materials, or innovative construction methodologies where technical failures could trigger substantial completion costs exceeding original contract values.

Financial strength demonstrated through balance sheets, income statements, cash flow statements, and working capital analysis affects underwriting decisions for larger bond amounts, with sureties examining asset quality, debt levels, profitability trends, and liquidity positions when evaluating applications for bonds exceeding several hundred thousand dollars. Contractors with strong balance sheets showing positive working capital, manageable debt ratios, consistent profitability, and substantial liquid assets receive more favorable premium quotes than contractors with negative working capital, excessive leverage, inconsistent earnings, or asset concentrations in illiquid real estate or equipment suggesting financial distress that could lead to business failures triggering bond claims.

How to Get Your Performance Bond

Obtaining your performance bond begins with identifying the specific bond amount and coverage requirements specified in contract documents, bid invitations, or regulatory statutes governing your construction project. Contact specialized surety bond agencies like Swiftbonds that maintain relationships with multiple surety companies capable of issuing performance bonds across all project sizes, construction types, and contractor experience levels, providing access to competitive markets and expert guidance navigating complex bonding requirements unique to your project and jurisdiction.

The application process involves submitting documentation including business and personal tax returns, financial statements showing assets and liabilities, personal financial statements for business owners and guarantors, credit authorization forms allowing sureties to pull credit reports, construction experience summaries detailing previously completed projects, current work schedules listing ongoing projects and available capacity, bank reference letters confirming relationships and account standings, and details about the specific project requiring bonding including contract amount, scope of work, project timeline, and owner identity. Sureties underwrite applications by evaluating creditworthiness through credit score analysis, examining financial strength through balance sheet review, assessing construction experience and professional qualifications, reviewing specific project requirements and technical complexities, and determining appropriate premium rates based on overall risk assessments.

Once underwriting concludes, sureties provide premium quotes typically ranging from one percent to three percent of bond amounts for qualified contractors with strong credit and established construction businesses, with higher rates for contractors facing credit challenges or operating newer ventures with limited track records. After accepting quoted terms and paying premiums, you receive bond documents that must be filed with obligees according to their specified procedures and deadlines to satisfy bonding requirements and secure final contract awards authorizing project commencement.

Swiftbonds LLC

2025 Surety Bond Technology Provider of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

The Performance Bond Default Process and Surety Remedies

When contractors fail to complete projects according to contract specifications, miss critical schedule milestones, deliver defective work violating building codes, or otherwise breach contractual obligations, project owners may file claims against performance bonds seeking financial compensation or completion assistance.

The claim process begins with project owners providing written notice to surety companies documenting contractor defaults and specifying claimed damages or completion costs resulting from contractor failures. Sureties investigate claims by reviewing contract documents, inspecting work completed to date, interviewing project owners and contractors to understand disputed issues, hiring independent experts to assess technical aspects of alleged defects or code violations, and determining whether valid claims exist under bond terms warranting surety intervention.

If sureties conclude claims are valid, they possess several remedy options for addressing contractor defaults and protecting project owner interests. The surety may provide financing to the defaulting contractor enabling project completion if the contractor came close to finishing work and requires only modest financial assistance to overcome temporary cash flow problems. The surety may arrange for completion by hiring replacement contractors to finish remaining work, paying all costs exceeding amounts remaining in original contracts while seeking reimbursement from defaulting contractors for excess completion expenses.

The surety may negotiate arrangements with project owners where owners select replacement contractors to complete projects while sureties compensate owners for excess completion costs up to bond limits. The surety may simply pay project owners cash settlements equal to bond amounts or documented completion costs, whichever is lower, allowing owners to independently arrange project completion using surety payments.

Regardless of which remedy option sureties choose, they aggressively pursue complete reimbursement from defaulting contractors for all amounts paid on claims plus investigation costs, legal fees, completion contractor expenses, interest charges, and administrative costs through indemnity agreements creating legally enforceable debt obligations surviving business bankruptcies when business owners provided personal guarantees.

Frequently Asked Questions

What happens if multiple contractors default on the same project requiring bond claims exceeding the bond amount?

Performance bonds specify maximum liability limits equal to contract amounts or specified percentages, capping total available recovery regardless of how many valid claims arise from contractor defaults. If multiple subcontractors or the general contractor default creating aggregate losses exceeding the bond amount, available funds may be exhausted before all valid claimants receive full compensation. Sureties typically pay claims in the order received or pro-rate available bond proceeds among multiple claimants when total valid claims exceed bond limits. Project owners facing losses exceeding bond amounts must pursue additional recovery through litigation against defaulting contractors, though contractors triggering bond claims often lack financial resources to satisfy judgments making additional recovery unlikely. This limitation explains why some project owners require bonds exceeding one hundred percent of contract amounts or require contractors to maintain umbrella coverage supplementing standard performance bond protection.

Can contractors with bad credit or previous bond claims still obtain performance bonds for new projects?

Obtaining performance bonds with poor credit scores below six hundred, recent bankruptcies within the past five to seven years, or past bond claims proves extremely difficult but not impossible through specialized high-risk surety programs willing to work with contractors standard markets decline. Standard surety markets typically decline contractors with credit scores below six hundred, bankruptcies within the past seven years, past bond claims demonstrating performance failures, significant financial weaknesses like negative working capital or excessive debt, outstanding tax liens, or civil judgments. Specialized high-risk sureties may still provide coverage but at dramatically higher premium rates potentially reaching ten to twenty percent of bond amounts instead of the one to three percent that strong contractors pay with excellent credit. Some high-risk programs require collateral such as cash deposits equal to bond amounts, letters of credit from banks, or pledges of business or personal assets securing the surety’s position and providing immediate recourse if claims arise. Indemnitors with strong finances unrelated to your construction business such as creditworthy relatives or business partners might be required to co-sign indemnity agreements guaranteeing bonds and accepting joint liability for reimbursement obligations. Working with surety specialists experienced in high-risk markets and willing to advocate for your application provides the best chance of securing coverage when you face credit challenges.

How do performance bonds differ from payment bonds and why are both often required together?

Performance bonds and payment bonds serve complementary but distinct purposes with performance bonds guaranteeing project completion according to contract specifications while payment bonds guarantee contractors will pay all subcontractors, suppliers, and laborers for incorporated labor and materials. Project owners benefit from performance bonds protecting against contractor abandonment or defective work requiring costly remediation, while subcontractors and suppliers benefit from payment bonds ensuring compensation even when general contractors fail financially or refuse to pay valid invoices. Sureties commonly issue combined performance and payment bonds as single instruments with unified premiums covering both guarantees, recognizing that contractors likely to default on project completion obligations often simultaneously fail to pay subcontractors and suppliers creating dual exposures. Public construction projects almost universally require both bond types because mechanic’s liens cannot be filed against government property, leaving unpaid subcontractors and suppliers without traditional collection remedies if payment bonds don’t provide compensation. Private projects increasingly require both bonds as project owners recognize that unpaid subcontractors may abandon job sites or deliver defective work when not receiving timely payment, potentially disrupting project schedules and quality even when general contractors have not yet defaulted on completion obligations to owners.

Do performance bonds automatically renew each year or do contractors need to take action to maintain coverage?

Performance bonds remain in force for contract durations specified in bond terms rather than operating on annual renewal cycles common with insurance policies, typically terminating when projects complete satisfactorily and obligees release bond obligations after final inspections confirm work meets specifications and warranty periods expire. Unlike insurance policies renewing annually requiring premium payments to maintain continuous coverage, performance bonds issued for specific construction projects remain effective throughout project durations as long as contractors fulfill contractual obligations regardless of how long projects take to complete. However, contract changes extending project durations or increasing contract amounts create “overruns” representing additional exposure to sureties backing bonds, requiring sureties to bill contractors for additional premiums reflecting increased risk exposures from extended timeframes or enlarged scopes. Contractors should notify sureties immediately when anticipating overruns to obtain advance premium quotes and include additional bonding costs when billing owners for contract extensions or change orders. Multi-year service contracts requiring ongoing performance such as waste collection, recycling, snow removal, or facility maintenance may require renewable performance bonds with annual premium payments extending coverage through successive service periods, though these renewable bonds differ from traditional construction performance bonds issued for specific projects with defined completion dates. Long-term construction projects exceeding one year may require surety consent for contract extensions with sureties conducting interim financial reviews ensuring contractors maintain adequate financial strength to complete extended projects before approving continuations.

What happens to performance bonds when contractors face bankruptcy during project execution?

Contractor bankruptcies during project execution trigger automatic surety involvement as bankruptcy filings constitute events of default under performance bonds authorizing project owners to file claims seeking completion assistance or financial compensation for losses caused by contractor insolvencies. Sureties must decide quickly whether to complete projects using original contractors supported by surety financing, hire replacement contractors to finish remaining work, or pay project owners cash settlements allowing owners to independently arrange completion. The surety’s choice depends on project completion percentages, remaining work complexity, availability of qualified replacement contractors, and potential excess completion costs compared to bond limits. Federal bankruptcy law grants sureties special rights to complete bonded construction projects without automatic stay restrictions that normally prevent creditors from pursuing assets of bankrupt entities, recognizing the public interest in infrastructure completion and the unique surety-principal relationship distinguishing bonds from ordinary debts. Sureties completing projects may access retained contract proceeds held by owners, claims against owners for completed work, and equipment or materials at job sites, though bankrupt contractors’ other assets typically remain protected by bankruptcy proceedings preventing surety access for reimbursement collection. Personal guarantees from contractors’ owners surviving corporate bankruptcies create ongoing reimbursement exposure for individuals who signed indemnity agreements, potentially requiring personal asset liquidation or individual bankruptcy filings if surety completion costs exceed available resources.

Conclusion

Performance bonds represent three-party financial guarantees required by government agencies and private project owners as conditions for awarding construction contracts, ensuring bonded contractors complete projects according to specifications while providing financial recourse for project owners when contractors default on obligations through abandonment, insolvency, incompetence, or contractual breaches. The three-party structure distinguishes bonds from all other financial products, creating triangular relationships among principals who purchase bonds and assume unlimited reimbursement obligations, obligees who require bonds for project protection, and sureties who issue bonds guaranteeing principals’ contractual performance while expecting complete recovery of all claim payments through aggressive reimbursement enforcement against defaulting contractors.

Understanding that performance bonds protect third parties rather than bond purchasers helps contractors appreciate the serious nature of indemnity obligations created when obtaining bonds to satisfy project requirements. The reimbursement requirement distinguishing bonds from insurance means bond claims create debt obligations principals must repay including claim amounts, investigation costs, legal fees, completion expenses, and interest, with collection actions potentially including lawsuits, asset liens, garnishments, and personal guarantees surviving business bankruptcies when business owners co-signed indemnity agreements.

The Miller Act requiring bonds for federal construction exceeding one hundred thousand dollars and state Little Miller Acts imposing similar requirements for state-funded projects establish legal frameworks making performance bonds mandatory for most public construction in the United States. Private developers increasingly require performance bonds even when not legally mandated, recognizing that bonding requirements provide assurance that contractors have undergone rigorous financial underwriting by surety companies while creating immediate recourse mechanisms when contractors default without requiring project owners to pursue uncertain litigation.

Performance bond premiums typically ranging from one percent to three percent for qualified contractors with strong credit and established track records represent small percentages of total contract amounts but provide substantial protection for project owners investing millions of dollars in construction ventures where contractor defaults could create catastrophic losses threatening project viability. The underwriting process focusing on contractors’ creditworthiness, financial strength, construction experience, and project management capabilities ensures only qualified contractors capable of completing projects successfully can obtain bonds at reasonable rates.

Five Hidden Realities About Performance Bonds

The ancient Code of Hammurabi established around 1750 BC contained specific provisions requiring construction guarantors to assume personal liability for builder failures including provisions allowing property owners to enslave guarantors’ family members when builders abandoned projects or delivered structures that collapsed causing injuries, creating arguably the harshest surety bond enforcement mechanism in recorded history where modern contractors complaining about reimbursement obligations might consider themselves fortunate compared to their Mesopotamian predecessors facing literal bondage for performance failures.

The global construction surety bond market generates over fifteen billion dollars in annual premium volume with North American markets accounting for approximately sixty percent of worldwide bonding activity, reflecting the unique legal frameworks in the United States and Canada requiring extensive bonding for public construction projects while most other countries rely primarily on letters of credit or parent company guarantees rather than traditional surety bonds for construction financial guarantees.

Some European and Asian countries require performance bonds for non-construction activities including telecommunications spectrum licenses guaranteeing licensees will deploy networks within specified timeframes, pharmaceutical manufacturing permits guaranteeing producers will maintain quality standards and supply continuity, broadcasting licenses guaranteeing stations will provide public service programming, and environmental remediation projects guaranteeing companies will complete cleanup activities according to regulatory schedules, demonstrating that performance bond concepts extend far beyond construction applications.

The surety industry maintains mutual reinsurance agreements through organizations like the National Association of Surety Bond Producers allowing smaller sureties to underwrite large performance bonds exceeding their individual capacity limits by sharing risk exposures with other surety companies, enabling contractors to obtain multi-million-dollar bonds from regional sureties that individually could not support such large exposures without reinsurance support from national and international surety markets.

During the 2008 financial crisis, numerous contractors with previously excellent credit and strong balance sheets suddenly faced surety bond terminations when sureties conducted emergency financial reviews revealing dramatic working capital deterioration and asset value declines threatening contractors’ abilities to complete bonded projects, forcing many contractors out of public construction markets regardless of their technical competence when sureties refused to issue new bonds or renew existing coverage based solely on macroeconomic conditions beyond contractors’ control demonstrating the cyclical nature of surety credit markets.

Leave a Reply