Here’s a sobering reality: 75% of the average home’s construction cost goes directly to subcontractors, not the general contractor whose name appears on the sign. These specialized tradespeople—electricians, plumbers, framers, concrete workers—perform the actual work that transforms blueprints into buildings. Yet every year, thousands of these essential workers complete their jobs only to discover the general contractor can’t or won’t pay them. Enter the payment bond, a financial safeguard that has quietly protected billions of dollars in construction payments since the Great Depression.

Payment bonds serve as the invisible safety net beneath America’s construction industry. When a general contractor defaults on payment obligations, these bonds ensure that the people who actually swung the hammers, installed the wiring, and poured the concrete still receive their hard-earned money. Whether you’re a contractor bidding on a federal highway project, a subcontractor installing HVAC systems in a new school, or a materials supplier delivering concrete to a government building site, understanding payment bonds isn’t just helpful—it’s essential to protecting your financial interests.

What Is a Payment Bond?

A payment bond is a surety bond that guarantees all subcontractors, material suppliers, and laborers on a construction project will receive full payment for their work and materials, even if the general contractor defaults or goes bankrupt. Think of it as an insurance policy, though technically it’s not insurance—it’s a three-party financial guarantee that creates a safety net ensuring no one works for free on a bonded project.

When a general contractor secures a payment bond, they’re purchasing a guarantee backed by a surety company’s financial strength. This guarantee assures project owners, subcontractors, and suppliers that if the contractor fails to pay what’s owed, the surety will step in to make things right. The bond doesn’t eliminate the contractor’s financial responsibility—quite the opposite. It ensures accountability by providing an enforceable mechanism for recovering unpaid amounts.

The Three-Party Relationship

Every payment bond involves exactly three parties, each with distinct roles and responsibilities:

The Principal is the general contractor or prime contractor who purchases the bond. By entering into this agreement, the principal guarantees they will pay all subcontractors, suppliers, and laborers according to contract terms. The principal bears ultimate financial responsibility for any valid claims filed against the bond, meaning they must reimburse the surety for all claim payments plus fees and interest.

The Obligee includes the project owner who requires the bond, plus all subcontractors, suppliers, and laborers who have the right to file claims against it. For public projects, the obligee is typically a government agency—federal, state, county, or municipal. The obligee benefits from the bond’s protection without paying for it.

The Surety is the insurance company or financial institution that underwrites and issues the bond. The surety commits to paying valid claims up to the bond’s full amount, providing immediate financial relief to unpaid parties. However, the surety then pursues reimbursement from the principal, using the indemnity agreement the principal signed when obtaining the bond.

This three-party structure creates accountability while ensuring that legitimate claims get paid promptly, regardless of the principal’s financial situation at the time.

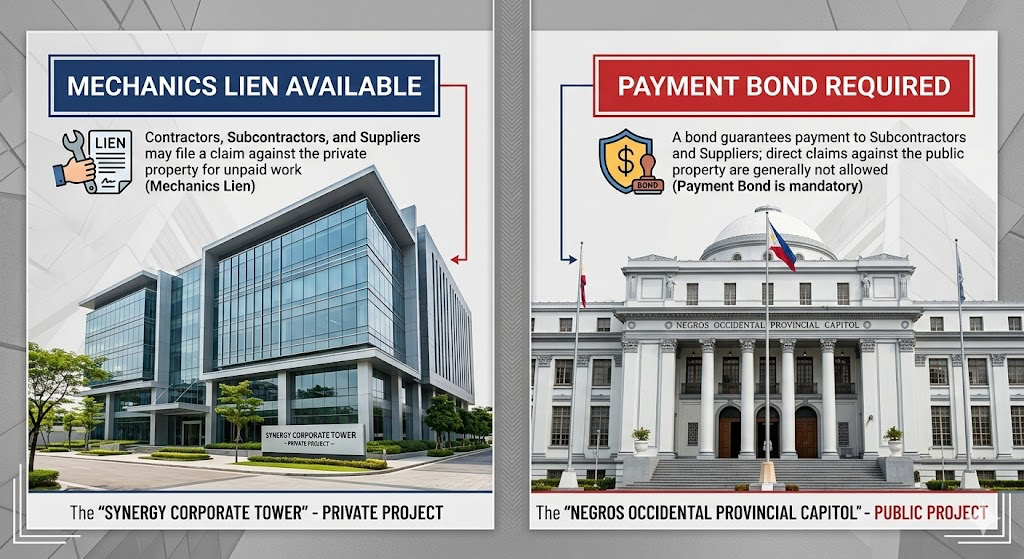

Why Payment Bonds Exist: The Mechanics Lien Problem

To understand why payment bonds matter so much in construction, you need to understand what happens on private versus public projects when contractors don’t get paid.

On a private commercial or residential project, an unpaid subcontractor or supplier has a powerful remedy: the mechanics lien. If you install $50,000 worth of electrical work in a new shopping center and don’t receive payment, you can file a lien against that property. This lien gives you a legal interest in the property itself—meaning the owner cannot sell, refinance, or transfer the property without first satisfying your lien. In extreme cases, mechanics liens can even force property foreclosure.

But what happens when you do electrical work on a new public school building and don’t get paid? You cannot file a mechanics lien. Government-owned property is immune from liens—you cannot place a lien on a courthouse, fire station, highway, or public school. This creates a massive problem: how do subcontractors and suppliers protect themselves when working on public projects?

The answer is payment bonds. These bonds serve as a substitute for mechanics lien rights on public projects. Instead of filing a lien against the property, unpaid parties file a claim against the payment bond. The surety investigates the claim and, if valid, pays it. This system protects taxpayer assets from liens while ensuring workers and suppliers still have recourse for nonpayment.

The Miller Act and Little Miller Acts

The legal foundation for payment bonds on public projects comes from the Miller Act, federal legislation passed in 1935 during the Great Depression. The Miller Act requires contractors on federal construction projects valued at $100,000 or more to furnish payment bonds equal to the contract amount. This law protects taxpayers by preventing liens on federal property while simultaneously protecting subcontractors and suppliers who contribute to these projects.

Every state has enacted its own version of the Miller Act, colloquially called “Little Miller Acts.” These state-level statutes establish payment bond requirements for state and local government projects. However, the specific requirements vary significantly from state to state.

| State Examples | Minimum Project Value | Bond Requirements |

|---|---|---|

| Texas | $25,000 | Required for state projects above threshold |

| Pennsylvania | $5,000 | Required for state projects above threshold |

| California | $25,000 | Required for public works projects |

| Florida | $200,000 | Required for public projects above threshold |

These varying thresholds mean contractors must understand the specific requirements in each jurisdiction where they work. Some states require bonds on projects as small as $5,000, while others only mandate them for contracts exceeding $200,000.

Private project owners aren’t legally required to demand payment bonds, but many do—especially on large commercial projects. Banks financing major developments often require payment bonds to protect their investment from potential lien complications.

Payment Bonds vs. Performance Bonds: Understanding the Difference

Payment bonds and performance bonds are almost always purchased together as a package called P&P Bonds, but they protect against entirely different risks:

Performance Bonds guarantee the contractor will complete the project according to contract specifications and within the agreed timeline. If the contractor abandons the project, performs substandard work, or fails to meet contract requirements, the performance bond ensures the work gets completed. The surety may hire a replacement contractor, provide financing for the original contractor to finish, or compensate the owner for losses.

Payment Bonds guarantee the contractor will pay everyone who contributes labor, materials, or services to the project. If the contractor doesn’t pay subcontractors or suppliers, the payment bond ensures these parties receive compensation.

Think of it this way: performance bonds protect the journey (getting the project built correctly), while payment bonds protect the people (ensuring everyone gets paid). A project owner needs both protections—assurance that the building will be completed as promised AND assurance that no mechanics liens or payment disputes will cloud the property title.

Here’s an important pricing note: when payment and performance bonds are issued together, they cost the same as purchasing just one bond. You essentially get both protections for the price of one, which is why they’re almost universally bundled together.

Who Needs Payment Bonds?

General contractors and prime contractors working on public projects almost always need payment bonds. Federal law requires them on contracts above $100,000, and state laws require them on state and local projects above varying thresholds. Even on private projects, contractors may need payment bonds if the project owner or financing institution requires them.

Subcontractors typically don’t purchase payment bonds themselves—they’re protected by the general contractor’s payment bond. However, on large projects, general contractors may require their major subcontractors to provide payment bonds guaranteeing payment to sub-subcontractors and material suppliers.

Project owners don’t purchase payment bonds but require contractors to provide them. Public agencies must require payment bonds on projects above statutory thresholds. Private owners choose whether to require them based on project size, financing requirements, and risk tolerance.

Material suppliers and laborers never purchase payment bonds—they’re the protected beneficiaries. These parties have the right to file claims against payment bonds when contractors fail to pay them.

The True Cost of Payment Bonds

Payment bond premiums typically range from 0.5% to 3% of the total contract value, with most falling between 1% and 2%. Several factors influence where your rate falls within this range:

Credit Score and Financial Strength: Contractors with excellent credit (750+) and strong financial statements receive the lowest rates, often below 1%. Those with fair credit (650-700) pay moderate rates around 1.5% to 2%. Contractors with challenged credit below 650 face rates of 2% to 5% or higher, and may struggle to find surety companies willing to bond them.

Experience and Track Record: Contractors with extensive experience in their specific construction niche and clean bonding histories receive preferred pricing. First-time bond applicants or those with previous claims against bonds pay higher rates reflecting increased risk.

Contract Size and Type: Smaller projects (under $500,000) often pay higher percentage rates but lower absolute amounts. Larger projects benefit from economies of scale with lower percentage rates. Specialized or high-risk work commands higher premiums than routine construction.

Bond Package: When payment and performance bonds are purchased together—which is nearly universal—the combined cost equals roughly what you’d pay for a performance bond alone. This bundling makes payment bonds essentially free when obtained with performance bonds.

For a $1 million construction contract with a contractor who has good credit and solid experience, expect to pay approximately $10,000 to $15,000 annually for combined payment and performance bonds.

Benefits for Subcontractors and Suppliers

Payment bonds provide critical protections for the tradespeople and material suppliers who make construction projects possible:

Guaranteed Payment Mechanism: When the general contractor fails to pay, you have a clear, enforceable path to compensation. File a valid claim, provide required documentation, and the surety must pay up to the bond amount.

Faster Resolution: Bond claims typically resolve much faster than litigation or mechanics lien foreclosure. Sureties have financial incentives to investigate and pay valid claims promptly.

No Property Ownership Risk: Unlike mechanics liens, payment bond claims don’t require you to potentially force foreclosure on property. The surety handles payment while you continue working.

Financial Strength Backing: Your payment isn’t dependent on a potentially insolvent contractor—it’s backed by a surety company with millions or billions in assets and strong financial ratings.

Professional Investigation: Sureties conduct thorough investigations of claims, often uncovering contractor misconduct and ensuring legitimate claims get paid even when the contractor disputes them.

Benefits for General Contractors

Contractors might view payment bonds as expensive hassles, but they provide significant business advantages:

Access to Projects: Without the ability to provide payment bonds, you’re automatically disqualified from all public work and most large private projects. Bonding capacity directly correlates with revenue capacity in the construction industry.

Subcontractor Confidence: Quality subcontractors prefer working with bonded general contractors because payment bonds guarantee their compensation. This access to the best subs improves your project quality and timeline performance.

Owner Trust: Payment bonds demonstrate financial stability and credibility. Project owners know that surety companies thoroughly vet contractors before bonding them, providing third-party validation of your qualifications.

Lien Protection: Payment bonds discourage and prevent mechanics lien filings. Even on private projects where liens are possible, the bond provides an alternative dispute resolution mechanism that keeps your projects clean.

Competitive Advantage: Building a strong bonding relationship and claim-free history allows you to bid on progressively larger projects, expanding your business capacity and revenue potential.

The Payment Bond Claims Process

When a subcontractor or supplier doesn’t receive payment, they must follow specific procedures to file a valid payment bond claim:

Send Preliminary Notice: Many states require preliminary notices sent at the project’s beginning, informing the owner, contractor, and surety of your work. Even when not legally required, preliminary notices establish your presence on the project and preserve your claim rights.

Send Notice of Intent: Before filing a formal claim, send a demand letter notifying the contractor and surety of your intent to file a bond claim unless payment is received. This final warning often prompts payment without formal claims.

File the Official Claim: Submit your bond claim according to state-specific requirements, typically via certified mail with return receipt. Include detailed documentation of work performed, materials supplied, payment terms, amounts owed, and proof of nonpayment.

Surety Investigation: The surety reviews your claim, examines contracts, verifies work completion, and investigates payment history. They may request additional documentation and interview involved parties.

Claim Payment or Denial: Valid claims receive payment up to the bond amount, typically within 30 to 90 days. Invalid claims receive written denial with explanation.

Enforcement: If your valid claim is wrongly denied, you may file suit against the bond to enforce payment. Most states require lawsuits within one year of project completion.

Understanding these steps ensures you preserve your rights and maximize your chances of successful claim resolution.

How to Get Your Payment Bond

Securing a payment bond follows a straightforward four-step process that typically takes just a few business days for qualified contractors.

Apply: Complete a surety bond application providing financial statements, project details, contract terms, and business history. Small bonds under $500,000 often require only basic information, while larger bonds demand comprehensive financial documentation including CPA-prepared statements, work-in-progress schedules, and detailed project histories.

Quote: The surety underwrites your application, evaluating your creditworthiness, financial strength, experience, and the specific project risks. You’ll receive a quote showing the bond premium (cost) and any special terms or conditions. Working with an experienced bond agent like Swiftbonds helps you compare multiple surety options to find the best rates and terms for your situation.

Pay: Accept the quote and pay the premium. Payment methods include wire transfer, ACH, credit card for smaller bonds, or premium financing for larger bonds where you pay in installments.

File: The surety issues your payment bond, which you file with the project owner or agency as specified in your contract. Keep copies for your records and note the bond’s effective dates and claim filing deadlines.

Swiftbonds LLC

2024 Surety Bond Provider of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

Bonding Capacity as a Revenue Cap

For contractors focused primarily on public work, payment bond capacity effectively caps your business growth. Surety companies extend bonding based on your financial strength, experience, and track record. This “bonding capacity” represents the maximum dollar value of bonded work you can have in progress simultaneously.

If your surety extends $5 million in bonding capacity, you cannot take on more than $5 million in bonded work at any given time. As you complete projects and free up capacity, you can bid on new work. But until then, you’ve reached your revenue ceiling regardless of market demand or your operational capability.

Growing your bonding capacity requires consistently strong financial performance, clean claim history, expanding equity, and building trust with your surety. Many contractors find that bonding capacity, not market opportunity or labor availability, becomes their primary growth constraint.

Special Considerations for Bad Credit

Contractors with credit challenges face significant hurdles obtaining payment bonds, but options exist. Some surety companies specialize in higher-risk contractors and will issue bonds with:

Higher Premiums: Expect rates of 3% to 10% compared to standard 1% to 2% rates. The increased cost reflects increased risk from the surety’s perspective.

Collateral Requirements: Sureties may require cash collateral, letters of credit, or pledged assets equal to 10% to 100% of the bond amount.

Smaller Bond Limits: Instead of $1 million or more in capacity, you might receive only $250,000 initially, growing as you prove reliability.

Indemnitors: Additional personal guarantees from business owners, officers, or even outside parties with strong financials may be required.

Joint Ventures: Partnering with a better-bonded contractor in joint venture arrangements can provide access to larger bonded projects while you build your own bonding capacity.

Don’t let credit challenges prevent you from bidding public work. Specialized bonding programs exist specifically for contractors rebuilding their credit and bonding history.

Frequently Asked Questions

Can I get a payment bond for a private project? Yes, though they’re not legally required. Private project owners often require payment bonds on large projects to protect against mechanics lien complications and ensure smooth project completion without payment disputes.

What happens if a subcontractor files a false claim? The surety investigates all claims thoroughly before payment. False claims are denied, and contractors making intentionally fraudulent claims may face legal consequences including criminal charges for fraud.

Do payment bonds cover change orders? Generally yes, provided the change orders were properly authorized and added to the contract scope. The payment bond typically covers the total contract value including approved changes.

How long does a payment bond remain active? Payment bonds typically remain in effect for the project duration plus a statutory claims period (often 1-2 years after project completion). State laws dictate specific timeframes for filing bond claims.

Can multiple subcontractors file claims on the same bond? Absolutely. Payment bonds cover all legitimate claims up to the total bond amount. If multiple parties file valid claims totaling more than the bond amount, payments may be prorated among claimants.

What if the contractor disputes my claim? The surety conducts an independent investigation regardless of the contractor’s position. Provide thorough documentation supporting your claim, including contracts, invoices, delivery receipts, lien waivers, and communication records.

Do I need separate bonds for each project? Yes, each bonded project requires its own payment and performance bonds. Bonds are project-specific, not blanket coverage for all your work.

Can payment bonds be canceled? Once issued and the project begins, payment bonds cannot be unilaterally canceled by the contractor or surety. They remain in effect for the full bond term unless the obligee provides written release.

Conclusion

Payment bonds form the financial backbone protecting America’s construction industry, ensuring that the tradespeople who build our infrastructure, schools, hospitals, and public buildings receive compensation for their labor and materials. These bonds bridge the gap created when mechanics liens aren’t available on public property, providing subcontractors and suppliers with enforceable payment guarantees backed by financially strong surety companies.

For general contractors, payment bonds open doors to public work and large private projects while building credibility with subcontractors and project owners. For subcontractors and suppliers, they provide security when working on projects where payment ultimately depends on third-party financing or government appropriations. For project owners and taxpayers, they ensure projects remain lien-free while holding contractors accountable for their payment obligations.

Understanding payment bonds—their purpose, mechanics, costs, and claims procedures—isn’t optional for construction professionals. Whether you’re bidding your first public project or managing your hundredth bonded job, this knowledge protects your financial interests and helps you navigate the complex web of relationships that make modern construction possible.

Five Fascinating Payment Bond Facts

The 80-20 Rule of Bond Claims: Industry data shows approximately 80% of all surety bond claims are filed against payment bonds rather than performance bonds. Despite both bonds being issued together, payment disputes far exceed performance failures, revealing that contractors struggle more with cash flow and payment management than with technical construction capability.

The Great Depression’s Lasting Legacy: The Miller Act passed in 1935 specifically because the previous law (the Heard Act of 1894) allowed contractors to use personal bonds from any surety, leading to widespread fraud during the Depression when thousands of undercapitalized “fly-by-night” sureties failed. The Miller Act’s requirement for Treasury-approved sureties created the modern surety industry.

Payment Bonds Predate Performance Bonds: Historically, payment bonds existed decades before performance bonds became standard. Early 20th-century public projects required only payment guarantees, assuming contractors would complete work to protect their reputations. Performance bonds only became universal after numerous project abandonments during economic downturns.

Federal vs. State Thresholds Tripled: The original Miller Act in 1935 required payment bonds on federal contracts exceeding $25,000—equivalent to roughly $550,000 today after inflation adjustment. The current $100,000 threshold means many smaller projects once requiring bonds now fall below the mandatory threshold, shifting risk to subcontractors.

Digital Bonds Are Transforming the Industry: Blockchain-based “smart bonds” are emerging that automatically trigger payment releases when milestones are met and verified through IoT sensors and project management software. These digital payment bonds reduce claim filing times from months to hours and may eventually eliminate payment disputes by creating self-executing payment guarantees tied directly to work verification.