Your general contractor just told you the government project requires both “liability insurance and performance bonds” before you can start the three-million-dollar highway expansion—then casually mentioned the bonds will cost you thirty thousand dollars that you must repay if anything goes wrong, while your insurance agent keeps insisting bonds and insurance are basically the same thing, leaving you completely confused about why you need both products that seem to provide identical financial protection. Understanding the fundamental differences between insurance policies that protect your business from unexpected losses and surety bonds that guarantee your performance to clients could mean the difference between securing lucrative contracts with proper financial planning and losing opportunities because you didn’t prepare for reimbursement obligations that could bankrupt your company if claims occur.

Insurance and surety bonds represent fundamentally different financial instruments serving distinct purposes despite both involving premium payments and risk management. Insurance policies create two-party contracts between businesses purchasing coverage and insurance companies providing protection, transferring risks of unpredictable events like fires, accidents, or lawsuits from policyholders to insurers who absorb losses without expecting repayment. Surety bonds establish three-party agreements among principals purchasing bonds, obligees requiring bonds for protection, and surety companies guaranteeing principals’ obligations, functioning as credit instruments where sureties temporarily pay claims but then aggressively pursue full reimbursement from principals who remain ultimately liable for all amounts paid plus investigation costs and legal fees.

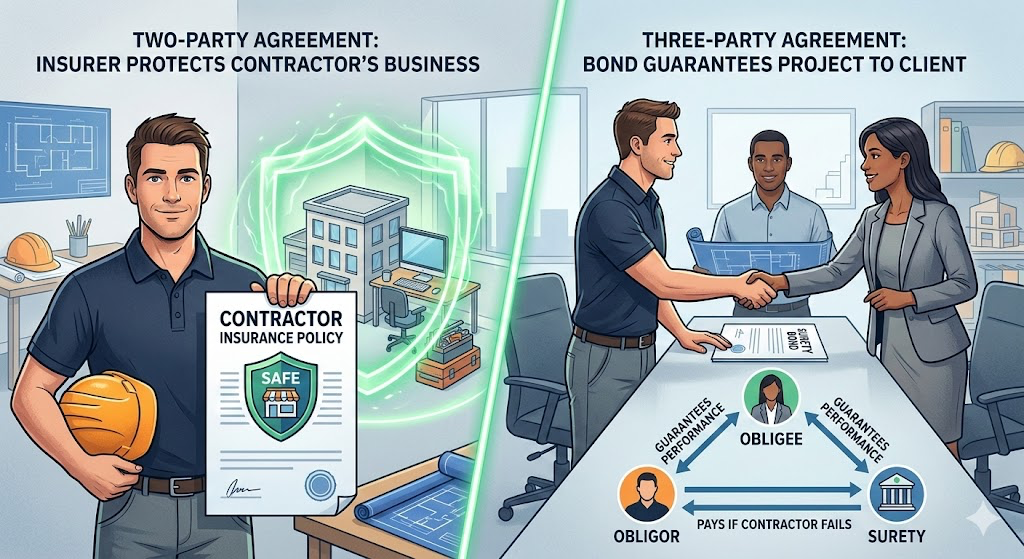

The Two-Party Versus Three-Party Structure

The foundational structural difference between insurance and surety bonds shapes every aspect of how these financial products operate, who they protect, and what obligations they create for businesses purchasing coverage.

Insurance policies involve two parties creating contractual relationships focused on protecting policyholders from financial harm. The insured party—your business, professional practice, or personal assets—purchases coverage from an insurance company that agrees to compensate you for specified losses occurring during policy periods. This bilateral agreement concentrates protection on the party paying premiums, creating no enforceable rights for third parties who might suffer damages from your actions. When covered events occur, you file claims directly with your insurer who investigates and pays according to policy terms without involving outside parties in the claim resolution process.

Surety bonds require three distinct parties with different roles, rights, and obligations under bond agreements creating more complex legal relationships than traditional insurance. The principal represents your business, contractor operation, or professional practice purchasing the bond and assuming complete financial responsibility for guaranteed obligations. You pay bond premiums to obtain coverage but receive no protection for yourself—instead, the bond exists solely to protect others from your failures to perform contractual duties or comply with regulatory requirements.

The obligee is the client, government agency, project owner, or regulatory authority requiring the bond as a condition of doing business, entering contracts, or maintaining licenses. Obligees benefit from financial guarantees that principals will fulfill obligations regardless of principals’ financial conditions or business failures. They can file claims against bonds when principals breach contracts, abandon projects, fail to pay subcontractors, or violate licensing laws, recovering financial losses directly from sureties without first pursuing principals through costly litigation.

The surety company issues bonds guaranteeing principals’ obligations to obligees, evaluating principals’ creditworthiness, financial strength, and performance capabilities before approval. Sureties maintain the financial reserves and legal authority to pay claims on principals’ behalf when obligations go unfulfilled, stepping into contractual relationships to either complete work, compensate obligees for losses, or arrange alternative performance. Unlike insurers who expect to absorb claim costs as part of their business model, sureties pursue complete reimbursement from principals for every dollar paid on claims plus all associated costs through indemnity agreements that create unlimited personal and corporate liability.

This three-party structure means surety bonds protect everyone except the party purchasing them, creating the counterintuitive reality that businesses pay premiums for financial products designed to protect their clients, customers, and regulators rather than themselves.

Who Actually Receives Protection

The direction of financial protection represents the most critical practical difference between insurance and surety bonds, determining who benefits when claims occur and who bears ultimate financial responsibility for losses.

Insurance policies protect businesses, professionals, and individuals purchasing coverage from financial losses they suffer due to covered events. When you buy general liability insurance, professional liability coverage, or property insurance, those policies exist to protect your business from claims, lawsuits, and losses that could otherwise devastate your finances. If customers slip and fall on your premises, if you make professional errors damaging clients, or if fires destroy your facilities, your insurance responds by paying claims on your behalf up to policy limits. The insurance company absorbs these losses as anticipated costs of doing business, pooling premiums from many policyholders to fund claims from the few who experience covered events.

You receive the financial benefit of insurance claim payments either through direct reimbursement for losses you suffered or through the insurer’s payment of judgments and settlements in lawsuits filed against you. The protection flows toward the party paying premiums, creating alignment between the purchaser’s interests and the coverage provided. This makes intuitive business sense—you buy protection to safeguard your own financial wellbeing from risks you face in operating your business.

Surety bonds protect obligees who require bonds rather than principals who purchase them, creating a fundamental disconnect between who pays for coverage and who benefits from protection. When government agencies require contractor license bonds, when project owners demand performance bonds, or when courts mandate fiduciary bonds, those bonds exist to protect the requiring parties from principals’ failures to meet obligations. The financial guarantee runs from principals through sureties to obligees, not back to principals purchasing coverage.

If you fail to complete a bonded construction project, abandon work after receiving payment, don’t pay subcontractors and suppliers as required, or violate licensing regulations, the project owner or government agency files claims against your bond seeking compensation for their losses. The surety investigates these claims and pays valid ones to make obligees whole for damages your failures caused them. You receive no benefit from these claim payments—instead, you face immediate demands from sureties for full reimbursement plus costs.

This protection direction creates the unusual situation where businesses must purchase and pay for financial products providing zero protection for themselves while creating contingent liabilities that can threaten their survival. Understanding this counterintuitive arrangement helps explain why surety bonds cost less than comparable insurance coverage—they’re not actually providing coverage to the party paying premiums but rather extending credit guarantees to third parties on the principal’s behalf.

Premium Structures and Payment Mechanisms

How premiums are calculated, collected, and utilized fundamentally differs between insurance and surety products, reflecting their different purposes and risk models.

Insurance premiums are designed to fund future claim payments across entire policyholder pools, with insurers collecting regular payments from many customers to create reserves covering losses suffered by the few experiencing covered events. When you pay monthly or annual insurance premiums for general liability, professional liability, or property coverage, those funds flow into large pooled accounts alongside premiums from thousands of other policyholders. Insurance companies invest these pooled funds to generate returns while maintaining sufficient liquidity to pay claims as they arise.

The premium amounts you pay reflect actuarial calculations estimating the likelihood and severity of claims your business might generate based on industry experience, your specific operations, claim history, and coverage limits selected. Insurers expect claims will occur and design premium structures to cover anticipated losses plus administrative expenses and profit margins. Higher-risk businesses or those with poor claim histories pay substantially higher premiums than lower-risk operations because insurers price coverage to reflect expected claim costs.

Insurance premiums typically require monthly or annual payments throughout policy periods, with coverage terminating if premium payments stop. This ongoing payment structure aligns with the continuous nature of insurance protection—you remain covered only as long as you continue paying premiums maintaining your policy in force.

Surety bond premiums represent one-time upfront payments covering specific bond terms, typically one year, rather than ongoing monthly obligations. When you purchase a fifty-thousand-dollar contractor license bond at a two percent rate, you pay a single one-thousand-dollar premium securing coverage for twelve months. This upfront payment differs fundamentally from monthly insurance premiums and reflects the credit-based nature of surety relationships rather than risk pooling.

Bond premiums do not fund future claim payments in the way insurance premiums do. Instead, premiums compensate sureties for underwriting costs, assumption of credit risk, and maintenance of financial reserves backing their guarantees. Sureties calculate premiums based on principals’ creditworthiness and likelihood of claim reimbursement rather than expected claim frequency or severity. Strong credit scores and solid financial statements yield low premium rates—often one-half to three percent of bond amounts—because sureties feel confident they can recover any claims they might pay.

Sureties intentionally price bonds at levels insufficient to fund claim payments because their business model assumes principals will reimburse all claims paid. This fundamentally different approach means surety premiums can remain much lower than insurance premiums for comparable coverage amounts since sureties don’t need to build claim reserves the way insurers do.

The one-time upfront premium structure means surety bonds don’t require ongoing monthly payments like insurance, though bonds must be renewed annually with new premium payments securing continued coverage for additional terms. Missing renewal premium payments causes bonds to lapse or cancel, potentially triggering license suspensions or contract defaults depending on bond requirements.

Claims Handling and Reimbursement Obligations

What happens when claims are filed against insurance policies versus surety bonds creates the starkest contrast between these financial products and generates the most significant financial consequences for businesses.

Insurance claims follow a straightforward process where policyholders notify insurers of covered events, insurers investigate to determine if claims fall within policy coverage, and insurers pay valid claims directly to injured parties or reimburse policyholders for covered losses up to policy limits. Once insurers pay claims, the matter concludes with no expectation that policyholders will repay the amounts insurers spent defending or settling claims. This one-way payment flow represents the core value proposition of insurance—transferring financial risks from businesses to insurers who absorb losses as their business function.

The lack of reimbursement obligations means insurance claims, while inconvenient and potentially resulting in premium increases or coverage cancellations, don’t create debt obligations or ongoing financial liability for policyholders beyond their premium commitments. When your general liability insurance pays a hundred-thousand-dollar slip-and-fall claim, you don’t owe your insurer one hundred thousand dollars. The insurer absorbed that loss as part of the risk they assumed when issuing your policy.

Surety bond claims create completely different financial dynamics where principals must ultimately reimburse sureties for all amounts paid on claims plus investigation costs, legal fees, and interest charges. When obligees file claims against your bonds alleging you failed to complete contracted work, didn’t pay subcontractors, or violated licensing requirements, sureties investigate these allegations but maintain absolute rights to pursue reimbursement if claims prove valid.

The claims process typically begins with sureties notifying principals of filed claims and requesting documentation supporting principals’ defenses. Sureties expect principals to either resolve claims directly with obligees, defend against claims by proving obligations were fulfilled, or explain circumstances that might invalidate claims. If principals cannot resolve situations or convince sureties that claims lack merit, sureties must decide whether to pay claims to protect their obligations to obligees.

When sureties pay claims—whether to compensate obligees for uncompleted work, reimburse them for financial losses, or arrange alternative contractors to complete projects—they immediately turn to principals demanding full reimbursement under indemnity agreements signed when bonds were obtained. These indemnity agreements create legally binding obligations requiring principals to repay sureties every dollar spent on claims regardless of whether principals have the financial resources to make payments.

The reimbursement demand includes not just the claim amount paid to obligees but also all costs sureties incurred investigating claims, legal fees for attorneys who reviewed bond language and advised on surety obligations, costs of arranging completion contractors if sureties chose that remedy, and interest accruing from payment dates until principals reimburse all amounts owed. A thirty-thousand-dollar claim payment might generate total reimbursement demands exceeding forty thousand dollars after adding investigation and legal costs.

Principals who cannot immediately reimburse sureties face aggressive collection actions including lawsuits, liens against business and personal assets, garnishment of accounts, and pursuit of personal guarantees from business owners and their spouses who co-signed indemnity agreements. These collection efforts can continue for years and survive business bankruptcies since indemnity obligations often involve personal guarantees extending beyond corporate liability protections.

This fundamental reimbursement difference means surety bonds function more like guaranteed loans than insurance, with sureties acting as financial backers who temporarily cover principals’ obligations but maintain absolute rights to recover all amounts advanced plus costs and interest.

Risk Types and Claim Expectations

The nature of risks covered and whether claims are expected or unexpected distinguishes insurance from surety bonds at a conceptual level affecting pricing, underwriting, and business models.

Insurance addresses unpredictable events that may or may not occur and largely fall outside policyholders’ direct control. Fires destroying business property, customers slipping on wet floors, professional errors causing client losses, or cyber criminals breaching computer systems represent uncertain risks that even well-managed businesses can experience. You cannot guarantee your building will never catch fire, that no customer will ever fall on your premises, or that employees will never make mistakes harming clients. These unpredictable calamities justify insurance protection since you cannot prevent all covered events through diligence alone.

Insurance companies expect claims will occur across their policyholder pools and price premiums to fund anticipated losses. Actuaries analyze historical loss data predicting that certain percentages of policyholders will file claims each year, allowing insurers to calculate premiums sufficient to pay expected claims while generating profits. The business model assumes losses will happen and builds claim payments into the fundamental economics of insurance operations.

Surety bonds guarantee defined performance that principals should accomplish and largely control through their own actions and decisions. Completing construction projects according to contract specifications, paying subcontractors and suppliers for work performed, complying with licensing laws and regulations, or fulfilling fiduciary duties represent obligations entirely within principals’ control assuming they have adequate resources, competence, and integrity. You can guarantee you’ll complete work if you manage projects properly, pay bills if you maintain sufficient cash flow, and follow laws if you understand regulatory requirements.

Sureties expect claims will not occur under normal circumstances since principals control whether they fulfill guaranteed obligations. The bonding business model assumes principals will perform as promised, with bonds serving as assurance mechanisms rather than anticipated claim funding vehicles. This expectation of performance rather than default explains why bond premiums can remain much lower than insurance premiums—sureties don’t need to price bonds anticipating claim payments the way insurers price policies expecting losses.

When surety bond claims do occur, they typically indicate serious problems with principals’ finances, competence, or integrity that prevented them from controlling outcomes they should have controlled. Contractor bankruptcies, abandonment of projects after receiving payment, fraud, or gross mismanagement create most surety claims rather than random uncontrollable events. This performance-based risk model means sureties investigate principals’ capabilities thoroughly before issuing bonds, declining applicants who appear likely to default on guaranteed obligations.

The fundamental difference between unpredictable insured risks and controllable bonded obligations shapes everything about how these products work and what they cost. Insurance pricing reflects anticipated random losses while bonding pricing reflects credit risk and reimbursement likelihood.

Coverage Scope and Specificity

How broadly or narrowly financial protection extends reveals another key distinction between insurance policies and surety bonds affecting how businesses structure their risk management programs.

Insurance policies typically provide broad coverage across entire business operations under single policies designed to address wide ranges of related risks. When you purchase general liability insurance, a single policy covers all bodily injury and property damage claims arising from your business operations regardless of specific projects, locations, or contracts involved. Your policy protects you whether injuries occur at your main office, a job site, a client location, or anywhere else your business activities create exposure.

This broad coverage means most businesses need relatively few insurance policies to address their major risk categories. A typical contractor might carry general liability covering all operations, professional liability for design or consulting work, workers compensation for employee injuries, commercial auto for vehicle accidents, and perhaps cyber liability for data breaches. Five or six policies can provide comprehensive coverage across all business activities.

Insurance policies remain in force continuously throughout policy periods covering all qualifying events that occur while coverage is active. You don’t need separate insurance policies for each project you undertake, each client you serve, or each location where you operate. The same general liability policy responds whether you’re working on one project or one hundred simultaneous jobs.

Surety bonds provide narrow specific coverage tied to particular obligations, contracts, licenses, or projects rather than broad protection across entire operations. When you obtain a contractor license bond, that bond guarantees only your compliance with licensing laws and regulations—it doesn’t guarantee you’ll complete any specific construction project. When you secure a performance bond for a particular highway project, that bond covers only that single project and provides no protection for other work you might perform simultaneously.

This specific nature means businesses often need multiple bonds active at the same time covering different obligations. A contractor might maintain a license bond required by the state, separate performance and payment bonds for each active construction project, bid bonds for projects they’re pursuing, and perhaps maintenance bonds for completed work still under warranty. Ten or twenty simultaneous bonds are not unusual for active contractors pursuing multiple projects.

Each bond addresses a distinct obligation with separate bond amounts, premium calculations, and claim exposures. Your license bond might be ten thousand dollars, while project-specific performance bonds could range from fifty thousand to several million dollars depending on contract values. Every new project or obligation requires obtaining additional bonds beyond those already in place.

The specific nature of surety bonds means coverage doesn’t automatically extend to new activities the way insurance typically does. Starting a new project, obtaining a new license, or entering a new contract requires securing appropriate new bonds rather than relying on existing coverage to protect new exposures.

How to Get Your Surety Bond

Getting your surety bond requires working with specialized surety professionals who understand bonding requirements and underwriting standards that differ substantially from insurance processes. Start by identifying the specific bond type you need—contractor license bonds, performance bonds, payment bonds, bid bonds, or commercial bonds—and determining the required bond amount specified by obligees in contract documents, licensing statutes, or project specifications. Contact surety bond agencies like Swiftbonds that focus exclusively on bond products and maintain relationships with multiple surety companies capable of issuing various bond types across different industries and risk profiles.

The application process involves submitting detailed financial documentation including business tax returns, financial statements, personal financial statements for owners, credit authorization forms allowing sureties to pull credit reports, and project-specific information if seeking contract bonds for construction or other performance obligations. Sureties underwrite applications evaluating your creditworthiness through personal and business credit scores, analyzing financial strength through balance sheet review assessing working capital and debt ratios, examining your experience and past performance completing similar obligations, and reviewing the specific obligation being bonded including contract terms and project complexity. Once underwriting concludes, sureties provide premium quotes typically ranging from half a percent to three percent of bond amounts for qualified applicants, with higher rates for those with credit challenges or weaker financials. After accepting quoted terms and paying premiums, you receive bond documents that must be filed with obligees according to their specified procedures and deadlines to satisfy bonding requirements.

Swiftbonds LLC

2025 Surety Bond Technology Provider of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

When Each Product Is Required or Recommended

Understanding when you must carry insurance versus when bonds are necessary helps businesses plan financially and maintain compliance with legal and contractual requirements.

Insurance requirements typically stem from three sources creating different levels of compulsion. State and federal laws mandate certain insurance types including workers compensation in most states, commercial auto liability in all jurisdictions, and unemployment insurance in every state. These statutory requirements leave no discretion—you must carry specified coverage as a condition of legal business operation regardless of your preferences or risk tolerance.

Contractual requirements impose insurance obligations when clients, lenders, landlords, or business partners demand coverage as conditions of doing business. General contractors require subcontractors to carry liability insurance naming them as additional insureds. Commercial leases require tenants to maintain property insurance protecting landlords’ interests. Lenders demand property insurance on financed equipment or real estate. These contractual mandates arise from the other party’s desire for protection rather than legal requirements.

Voluntary insurance represents coverage businesses purchase for their own protection even without legal or contractual mandates. Professional liability insurance, cyber liability coverage, business interruption protection, and excess liability policies typically fall into voluntary categories where businesses decide whether protection justifies premium costs. Sound risk management might recommend voluntary coverage even when nobody requires it.

Surety bond requirements almost always stem from legal mandates or contractual demands rather than voluntary purchases for self-protection. Government agencies require contractor license bonds, permit bonds, and various commercial bonds as licensing conditions under state statutes and local ordinances. These regulatory requirements leave no choice—you cannot obtain or maintain required licenses without posting bonds in amounts and forms specified by regulations.

Contract surety bonds including performance bonds, payment bonds, and bid bonds arise from project owners or general contractors requiring bonding as conditions of awarding contracts. Public construction projects operating under Miller Act and Little Miller Act statutes mandate performance and payment bonds by law. Private projects increasingly require bonds even without legal mandates because sophisticated owners recognize the protection bonding provides.

Court bonds mandated by judges in litigation or probate proceedings represent another category of legally required bonding where courts condition certain rights or privileges on posting bonds protecting other parties from potential losses. Appeal bonds, injunction bonds, fiduciary bonds, and guardianship bonds fall into this mandatory category.

The mandatory nature of most bonding requirements means businesses don’t choose whether to get bonded the way they might choose whether to buy certain insurance coverages. Bonding becomes a cost of doing business necessary to access opportunities, maintain licenses, or exercise legal rights rather than a voluntary risk management decision.

Frequently Asked Questions

If I have general liability insurance, do I still need surety bonds for my construction business?

Yes. General liability insurance and surety bonds serve completely different purposes and one cannot substitute for the other. Your general liability insurance protects your business from claims of bodily injury or property damage you cause to third parties during construction operations. Surety bonds guarantee to project owners that you’ll complete contracted work according to specifications, pay your subcontractors and suppliers, and fulfill other contractual obligations. Insurance addresses unpredictable accidents while bonds guarantee your performance of controllable obligations. Most construction projects require both insurance and bonds simultaneously since they address different risks and protect different parties.

What happens if I can’t repay the surety company after they pay a claim on my bond?

Sureties pursue aggressive collection actions including filing lawsuits against you personally and corporately, obtaining judgments allowing them to place liens on your business assets and personal property including your home if you provided personal guarantees, garnishing business bank accounts and accounts receivable, and potentially forcing business liquidation or personal bankruptcy if debts cannot be repaid. The indemnity agreements you signed when obtaining bonds typically include personal guarantees from business owners and their spouses, making everyone who signed personally liable for reimbursing all claim amounts plus costs and interest. These obligations survive business bankruptcies in many cases since personal guarantees extend beyond corporate liability protections. Inability to repay sureties can destroy your business, damage your personal credit for years, and create financial hardships affecting your family.

Can I purchase surety bonds directly from insurance companies or do I need a specialized bond agent?

While many insurance companies have surety divisions that issue bonds, working with specialized surety bond agencies or brokers typically provides better results than going directly to carriers. Surety bond specialists maintain relationships with multiple surety companies including those that might not write business directly with the public, understand which sureties offer the best programs for specific bond types or industries, can compare quotes from multiple carriers to find the lowest rates, and possess expertise navigating complex underwriting requirements that general insurance agents may not understand. Specialized bond professionals also better understand the credit-based nature of surety underwriting versus the risk-pooling approach of insurance, helping you present applications in ways that maximize approval likelihood and minimize premium costs.

Why do surety bonds cost so much less than insurance if they both provide financial guarantees?

Surety bonds cost dramatically less than comparable insurance coverage because sureties don’t expect to pay claims and don’t need to build reserves funding future losses the way insurers do. A one-million-dollar performance bond might cost ten to thirty thousand dollars annually while one million dollars of general liability insurance could cost fifty to one hundred thousand dollars or more. This pricing difference reflects fundamentally different business models—insurers price policies expecting they’ll pay claims and need premiums sufficient to fund those anticipated losses plus expenses and profits. Sureties price bonds expecting principals will perform as guaranteed with bonds rarely paying claims, needing premiums only to cover underwriting costs and compensation for credit risk assumed. When sureties do pay claims, they recover all amounts from principals through reimbursement, so premium revenue doesn’t need to fund claim payments.

If my business declares bankruptcy, am I still liable to repay surety claims?

Personal guarantees and indemnity agreements signed when obtaining bonds typically survive corporate bankruptcies, leaving individual guarantors personally liable for reimbursing sureties even after business entities discharge debts through bankruptcy proceedings. If you personally guaranteed your business’s bonds by signing indemnity agreements as most owners must, the surety can pursue you individually for claim reimbursement regardless of what happens to the corporate entity. Your personal assets including your home, retirement accounts, vehicles, and other property can be targeted for collection even after your business ceases operations. Some principals attempt to discharge surety debt through personal bankruptcy, but courts often rule that fraudulent or negligent acts creating bond claims generate non-dischargeable debts that survive bankruptcy protection. The lesson is clear—treat bond obligations with extreme seriousness since they can follow you personally long after your business fails.

Can I get surety bonds if I have poor credit or have had past bond claims?

Obtaining bonds with poor credit or claim history proves extremely difficult but not impossible through specialized high-risk surety programs. Standard surety markets decline applicants with credit scores below six hundred, recent bankruptcies, past bond claims, or significant financial weaknesses. Specialized high-risk sureties may still provide coverage but at dramatically higher premium rates potentially reaching ten to twenty percent of bond amounts instead of the one to three percent that strong applicants pay. Some high-risk programs require collateral such as cash deposits, letters of credit, or pledges of business or personal assets securing the surety’s position. Indemnitors with strong finances unrelated to your business might be required to guarantee bonds. Past bond claims create particularly difficult underwriting challenges since they demonstrate exactly the performance failures that bonds guarantee against, making sureties extremely reluctant to extend new credit to principals who previously defaulted.

What’s the difference between being bonded and insured, and why do businesses say they’re both?

Being bonded means you’ve obtained surety bonds guaranteeing your performance of contractual or regulatory obligations to protect your clients, customers, or regulators from your failures. Being insured means you’ve purchased insurance policies protecting your business from financial losses you suffer due to accidents, errors, or other covered events. Businesses advertise being “bonded and insured” to communicate they carry both financial protections simultaneously, signaling to potential clients that the business has been vetted by sureties willing to guarantee their work and maintains insurance protecting against operational risks. The dual status provides assurance that clients are protected if the business fails to perform (through bonds) while the business itself maintains financial stability to handle unexpected problems (through insurance). Both products require financial scrutiny to obtain, so businesses that are bonded and insured have passed underwriting reviews suggesting they’re financially stable and operationally competent.

How long does the surety bond approval process take compared to getting insurance?

Surety bond approval timelines vary dramatically based on bond types and applicant qualifications. Simple license bonds for financially strong applicants with excellent credit can be approved instantly online with bonds issued immediately upon premium payment. Complex contract bonds for construction projects or large bond amounts require extensive underwriting that can take days or weeks as sureties review financial statements, analyze project specifics, assess contractor experience, and potentially request additional documentation. Plan at least two to four weeks for major contract bonds if you’re a first-time applicant. Insurance approvals typically move faster since insurers don’t conduct the deep financial and credit analysis that sureties perform. Many insurance policies can be bound immediately with applications approved subject to final underwriting review, while surety bonds generally require complete underwriting approval before bonds are issued since sureties extend credit rather than pooling risk.

If I’m required to have both a performance bond and a payment bond, do I pay double the premium?

Not exactly double, but you do pay for both bonds since they’re separate guarantees addressing different obligations. Performance bonds guarantee you’ll complete work according to contract specifications while payment bonds guarantee you’ll pay subcontractors and suppliers. When both are required simultaneously as they typically are on public construction projects, sureties usually offer package pricing where the combined premium might be one and a half to one and three-quarters times what a single bond would cost rather than exactly double. For example, if a performance bond alone costs fifteen thousand dollars, getting both performance and payment bonds together might cost twenty-two to twenty-six thousand dollars rather than thirty thousand. The discount reflects administrative efficiencies and the fact that the same underwriting supports both bonds, but you definitely pay more for dual bonds than for a single bond.

Can my surety company cancel my bond in the middle of a project if they decide I’m too risky?

Surety companies generally cannot cancel contract bonds like performance and payment bonds mid-project once they’ve been issued and delivered to obligees, though cancellation provisions vary by bond type and jurisdiction. Most contract surety bonds are continuous or remain in effect until the bonded obligation is fully performed and the obligee releases the surety, preventing sureties from abandoning obligations partway through projects. License bonds and some commercial bonds may include provisions allowing sureties to cancel with advance notice periods typically ranging from thirty to ninety days, though even with these provisions, sureties remain liable for any obligations principals incur during the notice period. If sureties become concerned about your financial condition or project performance, they might refuse to issue new bonds for additional projects while maintaining existing bond obligations, effectively limiting your ability to take on new work without pulling coverage on current commitments.

Conclusion

Insurance and surety bonds represent fundamentally different financial products serving distinct purposes despite both involving risk management and premium payments. Insurance policies create two-party contracts protecting businesses purchasing coverage from unpredictable losses they suffer due to accidents, errors, or disasters, with insurers absorbing claim costs without expecting policyholders to reimburse paid amounts. Surety bonds establish three-party agreements guaranteeing principals’ obligations to obligees through sureties who temporarily pay claims but then aggressively pursue complete reimbursement from principals, functioning as credit extensions rather than risk transfers.

Understanding that insurance protects the party purchasing coverage while bonds protect third parties requiring guarantees helps businesses appreciate why both products are necessary for comprehensive risk management. The reimbursement obligation distinguishing bonds from insurance creates contingent liabilities that can threaten business survival if claims occur, making bond obligations far more serious than insurance claims that merely result in premium increases or coverage restrictions.

The credit-based nature of surety underwriting focusing on principals’ ability to repay claims differs dramatically from insurance underwriting that prices policies based on expected loss frequencies and severities. This difference explains why bonds cost less than comparable insurance coverage and why strong credit and solid financials prove essential for obtaining bonds at reasonable rates.

The specific narrow coverage of surety bonds addressing particular obligations contrasts with broad general coverage insurance provides across entire business operations. This specificity means businesses often need multiple simultaneous bonds covering different projects, licenses, and contracts while maintaining relatively few insurance policies addressing major risk categories.

Both insurance and surety bonds serve essential roles in modern business operations with insurance protecting businesses from financial devastation due to unexpected losses and bonds providing the financial guarantees necessary to access opportunities requiring performance or compliance assurances. Working with knowledgeable insurance professionals and specialized surety bond experts ensures businesses obtain appropriate coverage at competitive rates while understanding the obligations and exposures each product creates.

Five Critical Realities About Insurance Versus Surety Bonds Missing From Standard Comparisons

The historical origins of surety bonding dating back to the Code of Hammurabi in ancient Babylon around 1750 BCE reveal that performance guarantees through third-party sureties represent one of humanity’s oldest financial innovations, predating modern insurance by roughly three thousand years. Early Babylonian merchants posted sureties guaranteeing delivery of goods across dangerous trade routes, with wealthy guarantors pledging to compensate merchants if transporters failed to deliver cargo. This ancient practice evolved through Roman law’s concept of “fidejussio” allowing creditors to pursue guarantors for debtors’ obligations, medieval guild systems requiring master craftsmen to guarantee apprentices’ work quality, and English common law traditions establishing the legal framework that American surety law still follows today. Understanding surety’s ancient lineage helps explain why bonding operates through principles fundamentally different from insurance which emerged only in the seventeenth century.

The doctrine of “strictissimi juris” in surety law creates dramatically different claim defenses and legal interpretations than insurance contract law, with courts historically construing surety obligations strictly in favor of sureties while construing insurance policies strictly against insurers who drafted them. Under strictissimi juris, any material changes to bonded obligations—like contract modifications, deadline extensions, or scope alterations—can release sureties from liability entirely if principals and obligees modify agreements without surety consent. This strict construction principle means sureties can escape payment on technical grounds that wouldn’t relieve insurers from policy obligations, making surety bonds far less certain payment sources than insurance coverage despite both being financial guarantees. Modern commercial surety bonds often waive strict construction defenses, but understanding the doctrine helps explain why bond language must be followed precisely.

The unlimited joint and several liability created by surety indemnity agreements differs fundamentally from insurance’s limited policy protection, exposing all indemnitors to total claim amounts rather than proportional shares. When three business partners each owning one-third of a construction company sign surety bond indemnity agreements as co-indemnitors and a three-hundred-thousand-dollar claim occurs, the surety can pursue any single partner for the entire three hundred thousand dollars plus costs rather than limiting collection to one hundred thousand per partner. This joint and several liability means indemnitors cannot point to their percentage ownership arguing they should only reimburse proportional shares—each guarantor is individually responsible for one hundred percent of all surety losses. Insurance never creates similar exposure since policies protect purchasers rather than creating reimbursement obligations, demonstrating another profound difference in how these products allocate financial risk.

The absence of loss reserves and claim funds in surety accounting creates completely different balance sheet implications than insurance company financial structures, with sureties maintaining relatively minimal reserves since they expect to collect all claims from principals rather than absorbing losses. Insurance companies must establish and maintain massive loss reserves representing estimated future claim payments on policies already written, with actuaries calculating reserve requirements and regulators monitoring reserve adequacy to ensure insurers can pay all anticipated claims. Sureties maintain statutory reserves and surplus requirements but don’t build claim-specific reserves the way insurers do since their business model assumes zero net losses after principal reimbursements. This difference means surety companies can operate with dramatically less capital than insurance companies writing comparable coverage amounts, though sureties must demonstrate strong reinsurance relationships and access to capital markets if major claims exceed their immediate resources before principal reimbursements arrive.

The prequalification process unique to surety bonding where contractors and businesses establish bonding capacity before pursuing specific opportunities has no insurance equivalent and fundamentally shapes how bonded businesses approach growth and opportunity selection. Contractors seeking surety bonds for construction projects must first establish bond lines with sureties specifying single project limits representing the largest individual bond amounts sureties will issue and aggregate limits representing total bonded work principals can have active simultaneously. A contractor with a one-million-dollar single limit and three-million-dollar aggregate capacity can pursue individual projects up to one million dollars while maintaining up to three million in total bonded work across all active projects combined. This prequalification differs completely from insurance where businesses simply purchase needed coverage when projects arise rather than establishing capacity before opportunities emerge. The bonding prequalification requirement means contractors must build surety relationships and demonstrate financial strength before bidding bonded work, creating barriers to entry that don’t exist in insurance markets and fundamentally affecting business development strategies in bonded industries.