Your contractor just handed you a certificate labeled “bonded and insured” before starting your office renovation. You assumed both terms meant the same thing—some type of insurance protection. Three months later, the contractor abandons the half-finished project. You file a claim against their “bond” expecting immediate payment like insurance works, only to discover the surety company expects you to prove the contractor violated specific contract terms before they’ll investigate. That confusion between bonds and insurance just cost you weeks of delays and thousands in legal fees.

The Fundamental Difference Between Surety Bonds and Insurance

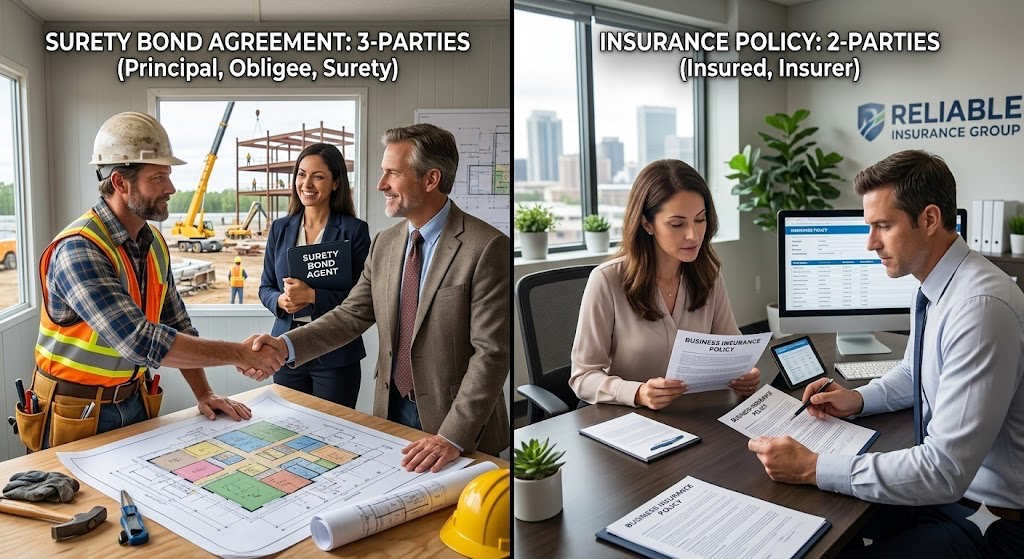

Surety bonds and insurance represent completely different financial instruments serving opposite purposes despite superficial similarities. Insurance functions as a two-party contract between you and an insurance company where you pay premiums to transfer risk away from your business, with the insurer paying claims without expecting reimbursement. Surety bonds create three-party agreements between you as the principal, the party requiring protection as the obligee, and the surety company guaranteeing your performance, with you remaining fully liable to reimburse the surety for any claims paid.

The most critical distinction centers on who receives protection. Insurance protects you—the policyholder—from financial losses caused by accidents, negligence, property damage, or unforeseen events that harm your business. When your liability insurance pays a slip-and-fall claim, that payment protects your business assets from lawsuit damages. Conversely, surety bonds protect others from you—specifically the obligee who contracts with you or relies on your regulatory compliance. When a performance bond pays a claim because you abandoned a construction project, that payment compensates the harmed project owner, not your business.

This opposite direction of protection explains why bonds require reimbursement while insurance does not. Insurance premiums pool risk across thousands of policyholders, with the insurance company expecting a certain percentage will file claims annually. The premium structure accounts for these anticipated losses, making reimbursement unnecessary. Surety bond premiums assume zero claims because surety companies carefully screen applicants and expect bonded parties to fulfill obligations. When bond claims occur, they represent failures the surety didn’t anticipate, triggering indemnity agreements that obligate you to reimburse every dollar paid plus expenses.

The three-party structure creates relationships that don’t exist in insurance. As the principal purchasing a bond, you promise the obligee that you’ll perform certain obligations or comply with specific regulations. The surety underwrites this promise based on your creditworthiness and ability to fulfill obligations, then guarantees payment to the obligee if you fail. This creates a unique situation where the surety simultaneously acts as your guarantor to the obligee and your creditor when claims arise. Insurance involves no such triangular relationship—just you and the insurer agreeing on premium payments and coverage terms.

How Surety Bonds Work: The Three-Party Agreement

Understanding each party’s role in the surety bond triangle clarifies why bonds differ fundamentally from insurance products. You serve as the principal, the party purchasing the bond and making the legal promise to fulfill specific obligations. These obligations might include completing a construction project per contract specifications, operating your business in compliance with state licensing regulations, or paying subcontractors and suppliers as agreed. Your decision to purchase the bond stems from external requirements rather than voluntary risk management.

The obligee represents the party requiring the bond and receiving protection from your potential failure. In construction, the obligee is typically the project owner or general contractor hiring you. For license bonds, the obligee is the government agency regulating your industry. The obligee does not pay for the bond or contribute premiums—they simply require it as a prerequisite for doing business with you or issuing licenses. This requirement shifts verification burden from the obligee to the surety company, essentially outsourcing due diligence to professional underwriters.

The surety company functions as the financial guarantor that underwrites your ability to fulfill obligations, issues the bond after approving your application, and guarantees payment to the obligee if you default. Major surety carriers include Travelers, Liberty Mutual, CNA, Hartford, and hundreds of smaller specialized companies. The surety investigates your credit history, financial statements, industry experience, and business track record before deciding whether to issue bonds. This underwriting examines not just the likelihood of claims but also your ability to reimburse the surety if claims occur.

When you sign bond applications, you also execute indemnity agreements making you personally liable for any surety payments regardless of business structure. These agreements survive business dissolution and bankruptcy, extending liability beyond the bonded entity. If your corporation defaults on a construction project triggering a one hundred thousand dollar bond claim, you personally owe the surety that amount even after closing the business. This personal liability creates powerful incentives to fulfill obligations and avoid bond claims at all costs.

The surety’s investigation and payment process differs dramatically from insurance claims. When obligees file bond claims, sureties investigate both parties, examining contracts, correspondence, change orders, payment records, and performance documentation. The surety defends you against fraudulent or exaggerated claims while also assessing whether legitimate violations occurred. This balanced investigation protects both you and the obligee, unlike insurance where the company defends only the policyholder. If claims are valid, the surety pays the obligee then pursues full reimbursement from you through the indemnity agreement.

How Insurance Works: The Two-Party Risk Transfer

Insurance operates through straightforward two-party agreements where you pay premiums to transfer specific risks from your business to the insurance company. These contracts outline covered perils, policy limits, deductibles, and exclusions that define when the insurer pays claims on your behalf. The relationship creates no obligations to third parties beyond the insurer’s promise to defend and indemnify you for covered claims within policy limits.

Insurance premiums reflect actuarial calculations estimating claim frequency and severity across all policyholders. The insurance company pools premiums from thousands of customers, invests these funds, and pays claims from the accumulated reserves. This pooled risk model expects a predictable percentage of policyholders will file claims annually, with premium calculations incorporating these anticipated losses. The mathematics work because most policyholders never file claims while a small percentage generate the losses covered by everyone’s premiums.

Claims under insurance policies trigger coverage when covered events occur—accidents, injuries, property damage, professional errors, or other specified perils. You notify the insurer of potential claims, provide documentation of the incident, and cooperate with their investigation. If the claim falls within policy coverage, the insurer pays settlements or judgments up to policy limits without expecting reimbursement from you. This unreimbursed payment represents the fundamental value proposition of insurance: transferring financial risk from you to the insurer.

The types of risks insurance covers differ fundamentally from bonded obligations. General liability insurance protects against accidents and injuries caused by your business operations, such as customers slipping on wet floors or contractors damaging client property during work. Professional liability insurance covers errors and omissions in services you provide, protecting against claims that your advice or work caused financial harm to clients. Property insurance reimburses you for damage to business assets from fire, theft, vandalism, or natural disasters. None of these coverages address your ability to fulfill contractual obligations or regulatory compliance—the domains where surety bonds operate.

Key Differences That Matter to Business Owners

| Aspect | Surety Bonds | Insurance |

|---|---|---|

| Parties Involved | Three parties (principal, obligee, surety) | Two parties (insured, insurer) |

| Who Is Protected | The obligee/third party/customer | The policyholder/business owner |

| Reimbursement | Principal must reimburse surety for all claims paid | No reimbursement expected from insured |

| Cost Structure | 1-5% of bond amount annually (upfront premium) | Regular premiums based on risk exposure |

| Purpose | Guarantee performance and compliance | Transfer risk from accidents and losses |

| Claims | Generally avoidable through compliance | Often unavoidable accidents/unforeseen events |

| Coverage Scope | Specific obligations or regulatory requirements | Broad protection against various perils |

| Underwriting Focus | Creditworthiness and ability to repay claims | Likelihood of accidents occurring |

| Legal Requirement | Often mandatory by law or contract | Some mandatory (workers comp), some voluntary |

| Financial Model | Line of credit (expects zero claims) | Risk pooling (expects regular claims) |

Understanding Premium Structures and Costs

Surety bond premiums function as fees for the surety’s credit extension and risk assumption rather than pre-funding for anticipated claims. When you purchase a ten thousand dollar performance bond for three hundred dollars, that premium compensates the surety for underwriting your application, monitoring the bond throughout its term, and assuming risk that you might default. The surety expects zero claims and prices accordingly, making bond premiums dramatically lower than equivalent insurance coverage.

Your credit score drives the majority of bond premium calculations because bonds function as unsecured lines of credit. Applicants with excellent credit above seven hundred twenty typically pay one to two percent of bond amounts annually. Good credit between six hundred fifty and seven nineteen pushes premiums to two to four percent. Fair credit from six hundred to six forty-nine results in four to seven percent rates, while poor credit below six hundred faces seven to fifteen percent premiums or outright declinations. This credit dependency reflects that sureties primarily worry about your ability to reimburse claims rather than claim likelihood.

Insurance premiums calculate differently, based on expected loss ratios across all policyholders in similar risk categories. Underwriters examine factors predicting accident frequency and severity—your industry, revenue, employee count, claims history, safety programs, and loss control measures. A contractor with five million in annual revenue might pay fifteen thousand dollars for general liability insurance because actuarial data shows contractors that size generate claims requiring coverage. The premium funds anticipated claims across all similar contractors, not your specific likelihood of filing claims.

The payment structures differ substantially between bonds and insurance. Most insurance requires monthly or annual premium payments throughout the policy term, with renewal premiums adjusting based on claims experience and changing risk factors. Surety bonds typically require single upfront premium payments for one-year terms, with no monthly installments or mid-term adjustments. Some surety providers offer financing for large bond premiums, but the bond itself represents a one-time purchase rather than ongoing premium obligations.

Common Types of Surety Bonds vs Insurance Policies

Construction performance bonds guarantee contractors will complete projects according to contract specifications, protecting project owners from contractor default, abandonment, or substantial defects. If contractors fail to perform, sureties either hire completion contractors to finish work or compensate owners for losses up to bond amounts. Payment bonds guarantee contractors will pay subcontractors, suppliers, and laborers, preventing mechanics liens on owner property when contractors don’t meet payment obligations.

License and permit bonds ensure businesses comply with regulations governing their industries, protecting consumers and government agencies from violations, fraud, or misconduct. Auto dealers post dealer bonds guaranteeing they’ll follow title transfer laws and consumer protection regulations. Contractors need license bonds before obtaining contractor licenses in most states. Collection agencies, mortgage brokers, and countless other regulated businesses must maintain license bonds as operating prerequisites.

General liability insurance protects businesses from third-party claims of bodily injury or property damage caused by business operations, products, or completed work. This coverage handles slip-and-fall accidents, property damage from contractor work, product defects causing injuries, and advertising injury claims. The insurance company defends lawsuits and pays settlements within policy limits without expecting reimbursement from the insured business.

Professional liability insurance, also called errors and omissions coverage, protects businesses providing professional services or advice from claims that negligent work caused client financial harm. Architects, engineers, consultants, accountants, and technology professionals typically carry professional liability coverage addressing mistakes, oversights, or failures to perform services as promised. This insurance covers legal defense and damages from malpractice or professional negligence claims.

Workers compensation insurance covers medical expenses and lost wages when employees suffer job-related injuries or illnesses, protecting employers from employee lawsuits over workplace injuries. Most states mandate workers compensation for businesses with employees, making it one of the few truly required insurance types. The coverage operates under no-fault principles where injured workers receive benefits regardless of who caused accidents.

When Businesses Need Both Bonds and Insurance

Construction contractors face the most comprehensive bonding and insurance requirements of any industry. Public construction projects almost universally require bid bonds guaranteeing contractors will enter contracts if awarded projects, performance bonds ensuring project completion, and payment bonds protecting subcontractors and suppliers. These contract surety bonds work alongside general liability insurance covering on-site accidents, workers compensation protecting employees, and builders risk insurance covering projects under construction.

The bonds and insurance serve completely different purposes on construction projects. Performance bonds protect owners from contractor default by guaranteeing project completion even if contractors abandon work or become insolvent. General liability insurance protects contractors from lawsuit costs when their work damages property or causes injuries. Neither coverage substitutes for the other—contractors need both to operate legally and protect against different categories of risk.

License bond requirements apply across industries from auto dealers and mortgage brokers to collection agencies and contractors. These bonds protect consumers and regulatory agencies from business misconduct, fraud, or violations of licensing regulations. The bonds guarantee financial recourse exists when businesses harm customers through illegal practices. Meanwhile, these same businesses need general liability insurance protecting against accidents and professional liability coverage addressing service errors.

Government contractors face extensive bonding requirements when bidding federal, state, or municipal contracts. The Miller Act mandates performance and payment bonds on federal construction projects exceeding certain thresholds. Many states have Little Miller Acts imposing similar requirements on state projects. These statutory bond requirements work alongside insurance mandates for general liability, workers compensation, and often professional liability coverage depending on contract scope.

The Claims Process: How Bonds and Insurance Differ

Insurance claims begin when policyholders notify insurers of incidents potentially covered by policies. You report slip-and-fall accidents, property damage, professional errors, or other covered events to your insurance company, providing documentation of what occurred. The insurer investigates by interviewing witnesses, examining evidence, consulting experts, and determining whether the incident falls within policy coverage. If covered, the insurer pays settlements or judgments without expecting reimbursement from you up to policy limits.

The insurance company’s investigation focuses on whether covered perils caused the claimed damages and whether any policy exclusions apply. Insurers defend you against fraudulent or exaggerated claims through their investigation and legal resources. The financial incentive aligns with protecting you because paying claims directly impacts their loss ratios and profitability. This creates a natural partnership where both you and your insurer want to minimize claim payments through effective defense.

Bond claims follow fundamentally different procedures because sureties protect obligees rather than principals. Obligees file claims directly with surety companies alleging principals violated bond conditions through contract defaults, licensing violations, or other specified misconduct. The surety investigates both parties impartially, examining contracts, performance records, payment histories, and communications to determine whether violations occurred. This balanced investigation differs from insurance where companies advocate exclusively for policyholders.

Sureties have no obligation to pay frivolous or exaggerated claims, defending principals against invalid allegations just as insurers defend policyholders. However, when investigations reveal legitimate violations, sureties pay obligees and immediately pursue reimbursement from principals through indemnity agreements. This reimbursement obligation fundamentally changes the claims dynamic—you want to avoid valid claims at all costs because you’ll personally repay every dollar the surety pays plus investigation expenses and legal fees.

How to Get a Surety Bond

Obtaining a surety bond requires a streamlined application process focused heavily on creditworthiness and financial stability. Start by identifying the specific bond type and amount your situation requires, whether a contractor license bond for ten thousand dollars, a performance bond for a construction project, or a commercial bond for regulatory compliance. Gather necessary documentation including business formation documents, financial statements for larger bonds, personal financial information, and details about the obligation being bonded.

Submit your application to a surety bond provider like Swiftbonds that specializes in your bond type and maintains relationships with multiple surety carriers. The application triggers credit checks on business owners, review of financial documents when required, and underwriting analysis determining your premium rate. Most straightforward applications for commercial bonds receive instant approval and quotes, while larger contract bonds may require several days for underwriting review and surety company approval.

Pay your bond premium once you accept the quote, using credit cards, ACH transfers, or financing arrangements for larger premiums. The surety issues your bond immediately after payment, providing the bond document electronically and often mailing the original for your records. File the bond with the obligee as required—some bonds require filing with government agencies, while others simply need to be maintained and provided to contract parties when requested.

Swiftbonds LLC

2024 Surety Bond Provider of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

Fast approval on commercial and contract bonds. Competitive rates for all credit levels. Expert guidance through the bonding process. Get your bond today.

Common Mistakes in Understanding Bonds vs Insurance

Assuming general liability insurance satisfies bonding requirements creates the most frequent and costly confusion among business owners. Contractors bidding projects often believe their insurance certificates prove they’re “bonded and insured” when they actually lack required performance or payment bonds. This assumption leads to contract violations, disqualification from bids, and lost opportunities when obligees specifically request bonds that don’t exist.

Believing bonds provide financial protection to the bonded party mirrors insurance thinking and misses the fundamental distinction. Business owners sometimes purchase bonds thinking they protect their companies from lawsuits or financial losses, only to discover bonds exclusively protect third parties. This confusion wastes money on unnecessary bonds when the business actually needs insurance coverage addressing their real risks.

Failing to understand reimbursement obligations creates catastrophic surprises when bond claims arise. Principals sometimes believe bond premiums function like insurance, pre-funding claims the surety will pay without recourse. When claims occur and sureties demand full reimbursement, principals face unexpected financial crises that insurance would have prevented. This misunderstanding often results from inadequate explanation during bond purchase about indemnity agreement implications.

Mixing terminology compounds confusion about which products provide which protections. Using “bonded” and “insured” interchangeably suggests they’re equivalent forms of protection when they serve opposite purposes. Clients requesting contractors be “bonded and insured” often can’t explain what each term means or which protections they actually need. This terminology confusion delays projects while parties clarify actual requirements.

Relying on bonds alone without appropriate insurance coverage leaves businesses financially vulnerable to the very risks insurance addresses. Some contractors maintain required performance bonds but skip general liability insurance to save money, exposing themselves to devastating lawsuit costs from on-site accidents. The bonds protect project owners but provide zero protection for the contractor’s business assets or personal finances.

Frequently Asked Questions

Can insurance replace surety bonds for construction projects?

No, insurance cannot replace surety bonds because they protect different parties and address different risks. Construction project owners require performance bonds specifically guaranteeing you’ll complete projects as contracted, with the surety stepping in if you default. Your general liability insurance protects you from accident lawsuits but provides no guarantee to project owners that you’ll finish work. Similarly, payment bonds protect subcontractors and suppliers from your failure to pay them, while your insurance offers them no such protection. Both bonds and insurance are necessary because each addresses distinct risks that the other doesn’t cover.

Why do I have to reimburse the surety if I already paid a premium?

Surety bond premiums compensate sureties for underwriting risk and extending credit guarantees, not for pre-funding anticipated claims like insurance. When you pay a three hundred dollar premium for a ten thousand dollar bond, that small fee reflects the surety’s expectation that you’ll fulfill obligations and generate zero claims. The premium funds administrative costs and risk assumption, not claim reserves. If claims occur despite the surety’s underwriting, you failed to perform as promised, triggering your indemnity agreement obligation to repay the surety. This reimbursement structure differs fundamentally from insurance where pooled premiums across all policyholders fund anticipated claims.

Do surety bonds cost more than insurance?

Surety bonds typically cost dramatically less than insurance on a per-dollar coverage basis because they serve different purposes. A ten thousand dollar performance bond might cost one hundred fifty to three hundred dollars annually, while ten thousand dollars of general liability insurance coverage is essentially impossible to price alone since liability policies start at much higher limits. However, comparing costs misses the point—bonds guarantee specific obligations while insurance transfers accident risks. Businesses need appropriate amounts of both rather than choosing based on cost. The combination of required bonds and necessary insurance creates the total protection cost businesses should budget.

Can I get bonds with bad credit or no credit history?

Businesses and individuals with poor credit can obtain surety bonds, though premiums increase substantially compared to good credit applicants. Sureties view credit as highly predictive of claim likelihood and repayment ability, charging rates from seven to fifteen percent of bond amounts for credit scores below six hundred. Some bond types prove harder to obtain with bad credit—large construction performance bonds may require collateral or be unavailable, while smaller commercial license bonds remain accessible through specialized high-risk programs. New businesses without credit histories face similar challenges, often needing personal guarantees from owners with established credit or potentially small amounts of collateral for larger bonds.

What happens to my business if I have a bond claim?

A valid bond claim creates immediate financial liability for the full claim amount plus all surety investigation and legal expenses. The surety pays the obligee according to the bond terms, then demands full reimbursement from you personally through your indemnity agreement. This reimbursement obligation survives business closure and bankruptcy, potentially pursuing you for years until paid. Additionally, bond claims make future bonding extremely difficult or impossible—most sureties decline applicants with bond claims within the past five years, while those who accept claims charge prohibitive premiums often exceeding twenty percent annually. A single significant bond claim often effectively ends businesses requiring bonds to operate.

Do I need bonds if I have a million dollar insurance policy?

Yes, high-limit insurance policies do not satisfy bonding requirements because bonds and insurance serve completely different purposes. Your million dollar general liability policy protects you from lawsuit costs when accidents occur, while bonds guarantee to third parties that you’ll fulfill specific obligations. Project owners requiring performance bonds need assurance you’ll complete their projects, which your liability insurance doesn’t provide. Regulatory agencies requiring license bonds need financial recourse if you violate regulations, which your insurance doesn’t offer them. The bond requirement exists independent of your insurance coverage, and one cannot substitute for the other regardless of policy limits.

How long does it take to get approved for a surety bond?

Most commercial surety bonds for amounts under fifty thousand dollars receive instant approval and issuance within hours when applicants have good credit and straightforward businesses. The application process involves credit checks on owners, basic business information verification, and automated underwriting that generates immediate quotes. Larger bonds, complex projects, or challenging credit situations require manual underwriting taking one to five business days. Construction performance bonds for major projects might need several weeks for surety company approval, financial statement reviews, and contract analysis. Starting the bond application early prevents last-minute delays when projects or licensing deadlines approach.

Can the same company provide both my bonds and insurance?

Many insurance agencies offer both insurance policies and surety bonds, though the products come from different divisions with separate underwriting. Your commercial insurance agent can often arrange bonds through their agency’s surety department or surety company relationships. However, the underwriting processes differ dramatically—insurance underwriters assess accident likelihood while bond underwriters focus on creditworthiness and financial strength. Some situations benefit from separating bond and insurance providers, particularly when your insurance carrier doesn’t offer competitive bond rates or your bonding needs require specialized surety expertise your insurance agent lacks.

What’s the difference between fidelity bonds and surety bonds?

Fidelity bonds technically function as insurance products despite the “bond” name, operating through two-party agreements between you and the bonding company. These bonds protect you from employee theft and dishonesty, reimbursing your business when employees steal money, property, or securities. Fidelity bonds operate like insurance with no reimbursement obligation—the bonding company pays valid claims without expecting repayment from you. Surety bonds create three-party agreements protecting third parties from your failures, with full reimbursement obligations when claims occur. The confusing terminology stems from historical naming conventions in the bonding industry that categorize some insurance products as “fidelity bonds.”

Are bonds tax deductible like insurance premiums?

Surety bond premiums are fully tax deductible as ordinary business expenses just like insurance premiums, since both constitute necessary costs of operating legally and obtaining contracts. The IRS treats bond premiums paid to obtain or maintain business licenses, fulfill contract requirements, or meet regulatory compliance as deductible business expenses. Report bond premiums on Schedule C for sole proprietorships or as business expenses for corporations and LLCs in the same tax categories as insurance premiums. Maintain premium receipts and bond documentation with tax records to substantiate deductions if questioned during audits. Consult your accountant about specific deduction timing if you prepay multi-year bond terms.

Conclusion

Surety bonds and insurance represent fundamentally different financial instruments that businesses frequently confuse despite serving opposite purposes in risk management. Insurance transfers accident and liability risks from your business to insurance companies through two-party contracts, with the insurer paying claims without reimbursement expectations. Surety bonds create three-party guarantees protecting third parties from your failures to fulfill obligations, with you remaining fully liable to reimburse sureties for any claims paid. Understanding these critical distinctions prevents costly mistakes like assuming insurance satisfies bonding requirements or believing bonds protect your business rather than your customers and contract partners. Successful businesses maintain appropriate levels of both bonds and insurance, recognizing that comprehensive protection requires addressing the different risk categories each product serves. The modest investment in proper bonding and insurance coverage prevents the catastrophic financial losses that single uninsured accidents or bond claims inflict on businesses operating without adequate protection.

Five Surprising Facts About Surety Bonds vs Insurance

The surety bond industry predates modern insurance by over four thousand years, with evidence of bonding arrangements in ancient Mesopotamia around 2750 BC. Archaeological discoveries revealed that Mesopotamian merchants used written guarantees where third parties pledged to fulfill obligations if primary obligors defaulted—the exact structure of modern surety bonds. Insurance as we know it developed much later, with marine insurance emerging in fourteenth-century Italy and property insurance expanding after the Great Fire of London in 1666. This four-thousand-year head start means surety bonding principles influenced early commercial law and contract enforcement long before insurance became widespread. The ancient roots explain why bonding feels more rigid and legally formal than insurance—it literally predates most modern legal systems.

The federal government serves as the world’s largest bond obligee, requiring surety bonds on over twenty-five billion dollars of federal construction projects annually. The Miller Act mandates performance and payment bonds on all federal construction contracts exceeding one hundred fifty thousand dollars, creating a massive government bonding market. In contrast, the federal government is a relatively minor insurance purchaser despite its size. This reversal occurs because government projects need performance guarantees that bonds provide, while government agencies self-insure many risks that private businesses transfer to insurance companies. The government’s dominance as a bond obligee shapes the entire surety industry’s standards and practices.

Surety companies must maintain capital and surplus ratios dramatically higher than property-casualty insurance companies despite writing far fewer policies. State insurance regulators require sureties to maintain premium-to-surplus ratios not exceeding ten to one, meaning a surety writing one hundred million in annual bond premiums needs at least ten million in capital and surplus. Property-casualty insurers can operate at three to one ratios or even higher. This conservative capital requirement reflects that bond claims can devastate sureties more than insurance claims affect insurers—when principals can’t reimburse claim payments, sureties absorb entire losses rather than spreading them across policyholder pools. The stricter capital requirements make surety companies more financially stable but also more selective about which bonds they’ll write.

Blockchain technology and digital bonds represent the surety industry’s most significant innovation since computerization, with several states now accepting electronic bond filing. Nevada became the first state allowing completely digital contractor license bonds in 2019, with California, Texas, and others following. These digital bonds exist entirely as cryptographic records on blockchain ledgers, eliminating physical bond forms, manual filing, and paper storage. The technology also enables instant verification that bonds remain active rather than requiring phone calls to surety companies. However, this innovation hasn’t reached insurance policies to the same degree because insurance focuses on ongoing coverage periods while bonds often serve short-term projects or annual licensing requirements better suited to blockchain’s transactional nature.

The surety industry experienced its worst losses in history during the 2008-2009 financial crisis despite having no direct exposure to mortgage securities or housing markets. Surety companies paid unprecedented claims when contractors bonded for construction projects went bankrupt during the recession, triggering performance bond obligations. The surety industry paid over four billion dollars in construction bond claims during 2009-2010, dramatically exceeding normal annual claims of several hundred million dollars. This crisis proved that surety bond losses track economic conditions and business failures rather than insurable events like natural disasters. Insurance companies also suffered losses during the crisis, but for completely different reasons—investment portfolio declines and increased liability claims from distressed businesses. The simultaneous but different crisis impacts on surety versus insurance reinforced how distinctly these industries operate despite surface similarities.

Leave a Reply